|

Sincerely,

|

|

|

|

|

David

A. Bochnowski

|

|

|

Chairman

and Chief Executive

Officer

|

|

|

December 31,

|

December 31,

|

December 31,

|

December 31,

|

December 31,

|

December 31,

|

||||||||||||||||||

|

Fiscal Year Ended

|

2009

|

2008

|

2007

|

2006

|

2005

|

2004

|

||||||||||||||||||

|

Statement

of Income:

|

||||||||||||||||||||||||

|

Total

interest income

|

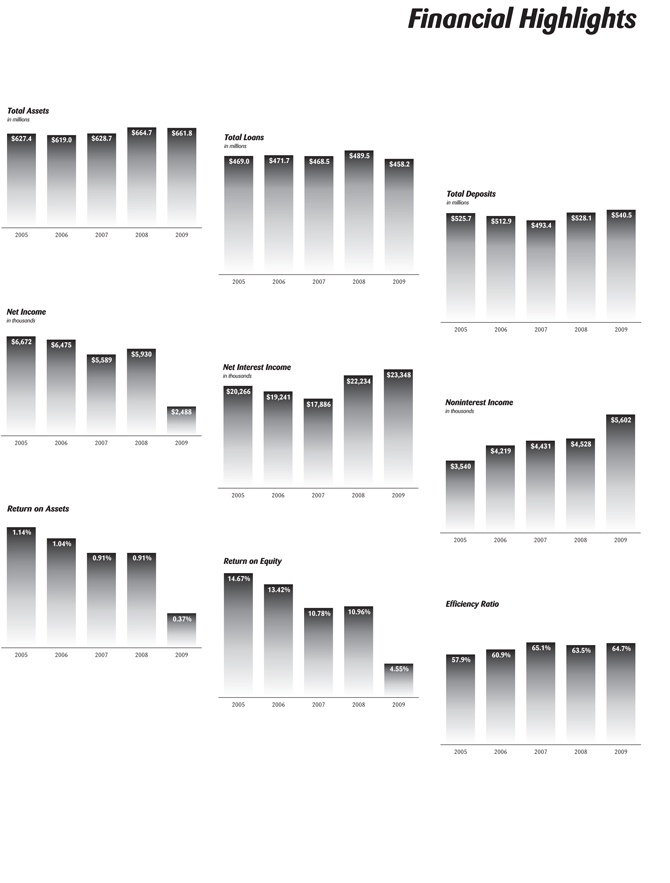

$ | 32,189 | $ | 35,167 | $ | 35,768 | $ | 34,979 | $ | 30,024 | $ | 26,614 | ||||||||||||

|

Total

interest expense

|

8,841 | 12,933 | 17,882 | 15,738 | 9,758 | 6,858 | ||||||||||||||||||

|

Net

interest income

|

23,348 | 22,234 | 17,886 | 19,241 | 20,266 | 19,756 | ||||||||||||||||||

|

Provision

for loan losses

|

8,540 | 2,388 | 552 | 15 | 245 | 385 | ||||||||||||||||||

|

Net

interest income after provision for loan losses

|

14,808 | 19,846 | 17,334 | 19,226 | 20,021 | 19,371 | ||||||||||||||||||

|

Noninterest

income

|

5,602 | 4,528 | 4,431 | 4,219 | 3,540 | 3,312 | ||||||||||||||||||

|

Noninterest

expense

|

18,735 | 16,999 | 14,525 | 14,296 | 13,771 | 13,174 | ||||||||||||||||||

|

Net

noninterest expense

|

13,133 | 12,471 | 10,094 | 10,077 | 10,231 | 9,862 | ||||||||||||||||||

|

Income

tax expenses/(benefit)

|

(813 | ) | 1,445 | 1,651 | 2,674 | 3,118 | 3,219 | |||||||||||||||||

|

Net

income

|

$ | 2,488 | $ | 5,930 | $ | 5,589 | $ | 6,475 | $ | 6,672 | $ | 6,290 | ||||||||||||

|

Basic

earnings per common share

|

$ | 0.88 | $ | 2.11 | $ | 1.99 | $ | 2.32 | $ | 2.40 | $ | 2.28 | ||||||||||||

|

Diluted

earnings per common share

|

$ | 0.88 | $ | 2.10 | $ | 1.98 | $ | 2.30 | $ | 2.37 | $ | 2.24 | ||||||||||||

|

Cash

dividends declared per common share

|

$ | 1.21 | $ | 1.44 | $ | 1.44 | $ | 1.40 | $ | 1.32 | $ | 1.24 | ||||||||||||

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

|||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

2004

|

|||||||||||||||||||

|

Balance

Sheet:

|

||||||||||||||||||||||||

|

Total

assets

|

$ | 661,806 | $ | 664,732 | $ | 628,718 | $ | 618,982 | $ | 627,439 | $ | 557,393 | ||||||||||||

|

Loans

receivable

|

458,245 | 489,509 | 468,459 | 471,716 | 469,043 | 433,790 | ||||||||||||||||||

|

Investment

securities

|

144,333 | 126,722 | 114,644 | 99,012 | 90,093 | 79,979 | ||||||||||||||||||

|

Deposits

|

540,527 | 528,148 | 493,384 | 512,931 | 525,731 | 451,573 | ||||||||||||||||||

|

Borrowed

funds

|

63,022 | 74,795 | 76,930 | 51,501 | 51,152 | 57,201 | ||||||||||||||||||

|

Total

stockholders’ equity

|

53,078 | 52,773 | 52,733 | 50,010 | 46,433 | 44,097 | ||||||||||||||||||

|

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

||||||||||||||||||

|

Fiscal

Year Ended

|

2009

|

2008

|

2007

|

2006

|

2005

|

2004

|

||||||||||||||||||

|

Interest

Rate Spread During Period:

|

||||||||||||||||||||||||

|

Average

effective yield on loans and investment securities

|

5.16 | % | 5.78 | % | 6.21 | % | 6.02 | % | 5.50 | % | 5.31 | % | ||||||||||||

|

Average

effective cost of deposits and borrowings

|

1.45 | % | 2.19 | % | 3.18 | % | 2.77 | % | 1.82 | % | 1.40 | % | ||||||||||||

|

Interest

rate spread

|

3.71 | % | 3.59 | % | 3.03 | % | 3.25 | % | 3.68 | % | 3.91 | % | ||||||||||||

|

Net

interest margin

|

3.74 | % | 3.65 | % | 3.10 | % | 3.31 | % | 3.71 | % | 3.94 | % | ||||||||||||

|

Return

on average assets

|

0.37 | % | 0.91 | % | 0.91 | % | 1.04 | % | 1.14 | % | 1.17 | % | ||||||||||||

|

Return

on average equity

|

4.55 | % | 10.96 | % | 10.78 | % | 13.42 | % | 14.67 | % | 14.64 | % | ||||||||||||

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

|||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

2004

|

|||||||||||||||||||

|

Total

capital to risk-weighted assets

|

11.5 | % | 12.0 | % | 12.0 | % | 12.0 | % | 11.6 | % | 12.2 | % | ||||||||||||

|

Tier

1 capital to risk-weighted assets

|

10.3 | % | 10.8 | % | 11.0 | % | 11.1 | % | 10.7 | % | 11.2 | % | ||||||||||||

|

Tier

1 capital to adjusted average assets

|

7.8 | % | 8.2 | % | 8.3 | % | 8.0 | % | 7.9 | % | 8.0 | % | ||||||||||||

|

Allowance

for loan losses to total loans

|

1.33 | % | 1.19 | % | 0.98 | % | 0.90 | % | 0.89 | % | 0.90 | % | ||||||||||||

|

Allowance

for loan losses to non-performing loans

|

32.93 | % | 46.97 | % | 53.16 | % | 153.95 | % | 198.00 | % | 371.00 | % | ||||||||||||

|

Non-performing

loans to total loans

|

4.05 | % | 2.54 | % | 1.84 | % | 0.58 | % | 0.45 | % | 0.24 | % | ||||||||||||

|

Total

loan accounts

|

4,846 | 5,193 | 5,268 | 5,392 | 5,422 | 5,370 | ||||||||||||||||||

|

Total

deposit accounts

|

32,616 | 33,692 | 30,760 | 32,435 | 33,963 | 32,866 | ||||||||||||||||||

|

Total

Banking Centers (all full service)

|

11 | 10 | 9 | 8 | 8 | 8 | ||||||||||||||||||

|

December 31,

|

December 31,

|

December 31,

|

December 31,

|

|||||||||||

|

2003

|

2002

|

2001

|

2000

|

|||||||||||

| $ | 26,357 | $ | 27,781 | $ | 28,425 | $ | 28,077 | |||||||

| 7,521 | 10,107 | 13,222 | 13,386 | |||||||||||

| 18,836 | 17,674 | 15,203 | 14,691 | |||||||||||

| 420 | 720 | 230 | 175 | |||||||||||

| 18,416 | 16,954 | 14,973 | 14,516 | |||||||||||

| 2,968 | 2,675 | 2,402 | 1,995 | |||||||||||

| 12,037 | 10,859 | 9,911 | 9,449 | |||||||||||

| 9,069 | 8,184 | 7,509 | 7,454 | |||||||||||

| 3,411 | 3,277 | 2,754 | 2,691 | |||||||||||

| $ | 5,936 | $ | 5,493 | $ | 4,710 | $ | 4,371 | |||||||

| $ | 2.16 | $ | 2.01 | $ | 1.73 | $ | 1.61 | |||||||

| $ | 2.13 | $ | 1.99 | $ | 1.71 | $ | 1.60 | |||||||

| $ | 1.20 | $ | 1.12 | $ | 1.04 | $ | 0.96 | |||||||

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

|||||||||||

|

2003

|

2002

|

2001

|

2000

|

|||||||||||

| $ | 508,775 | $ | 488,002 | $ | 440,710 | $ | 392,313 | |||||||

| 409,808 | 380,428 | 342,642 | 326,207 | |||||||||||

| 63,733 | 56,571 | 67,260 | 38,128 | |||||||||||

| 421,640 | 406,673 | 355,215 | 324,310 | |||||||||||

| 40,895 | 36,065 | 44,989 | 30,599 | |||||||||||

| 41,554 | 39,148 | 35,882 | 33,529 | |||||||||||

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

|||||||||||

|

2003

|

2002

|

2001

|

2000

|

|||||||||||

| 5.65 | % | 6.26 | % | 7.29 | % | 7.88 | % | |||||||

| 1.67 | % | 2.38 | % | 3.55 | % | 3.95 | % | |||||||

| 3.98 | % | 3.88 | % | 3.74 | % | 3.93 | % | |||||||

| 4.04 | % | 3.99 | % | 3.90 | % | 4.12 | % | |||||||

| 1.20 | % | 1.18 | % | 1.15 | % | 1.17 | % | |||||||

| 14.65 | % | 14.58 | % | 13.49 | % | 13.30 | % | |||||||

|

December

31,

|

December

31,

|

December

31,

|

December

31,

|

|||||||||||

|

2003

|

2002

|

2001

|

2000

|

|||||||||||

| 12.5 | % | 13.1 | % | 13.6 | % | 13.6 | % | |||||||

| 11.5 | % | 11.9 | % | 12.5 | % | 12.3 | % | |||||||

| 8.0 | % | 7.6 | % | 8.3 | % | 8.6 | % | |||||||

| 0.92 | % | 0.96 | % | 0.92 | % | 1.02 | % | |||||||

| 220.31 | % | 152.43 | % | 108.64 | % | 183.54 | % | |||||||

| 0.42 | % | 0.63 | % | 0.85 | % | 0.55 | % | |||||||

| 5,213 | 5,049 | 4,964 | 4,762 | |||||||||||

| 32,502 | 31,385 | 30,433 | 28,906 | |||||||||||

| 8 | 8 | 8 | 8 | |||||||||||

|

·

|

We

expect to face increased regulation of our industry. Compliance with such

regulation may increase our costs and limit our ability to pursue business

opportunities.

|

|

·

|

Our

ability to assess the creditworthiness of our customers may be impaired if

the models and approaches we use to select, manage and underwrite our

customers become less predictive of future

behaviors.

|

|

·

|

The

process we use to estimate losses inherent in our credit exposure requires

difficult, subjective and complex judgments, including forecasts of

economic conditions and how these economic predictions might impair the

ability of our borrowers to repay their loans, which may no longer be

capable of accurate estimation which may, in turn, impact the reliability

of the process.

|

|

·

|

Our

ability to borrow from other financial institutions on favorable terms or

at all could be adversely affected by further disruptions in the capital

markets or other events, including actions by rating agencies and

deteriorating investor

expectations.

|

|

·

|

Competition

in our industry could intensify as a result of the increasing

consolidation of financial services companies in connection with current

market conditions.

|

|

·

|

We

may be required to pay significantly higher deposit insurance premiums

because market developments have significantly depleted the insurance fund

of the Federal Deposit Insurance Corporation and reduced the ratio of

reserves to insured deposits.

|

|

Required for

|

To Be Well

|

|||||||||||||||||||||||

|

At December 31, 2009

|

Actual

|

Adequate

Capital

|

Capitalized

|

|||||||||||||||||||||

|

Amount

|

Ratio

|

Amount

|

Ratio

|

Amount

|

Ratio

|

|||||||||||||||||||

|

Total

capital to risk-weighted assets

|

$ | 58,689 | 11.5 | % | $ | 40,770 | 8.0 | % | $ | 50,963 | 10.0 | % | ||||||||||||

|

Tier

1 capital to risk-weighted assets

|

$ | 52,574 | 10.3 | % | $ | 20,385 | 4.0 | % | $ | 30,578 | 6.0 | % | ||||||||||||

|

Tier

1 capital to adjusted average assets

|

$ | 52,574 | 7.8 | % | $ | 20,112 | 3.0 | % | $ | 33,520 | 5.0 | % | ||||||||||||

|

|

Plante

& Moran, PLLC

|

|

|

Crowe

Horwath LLP

|

|

|

December 31,

|

|||||||

|

(Dollars in thousands)

|

2009

|

2008

|

||||||

|

ASSETS

|

||||||||

|

Cash

and non-interest bearing balances in financial

institutions

|

$ | 8,705 | $ | 10,005 | ||||

|

Interest

bearing balances in financial institutions

|

447 | 1,291 | ||||||

|

Federal

funds sold

|

4,070 | – | ||||||

|

Total

cash and cash equivalents

|

13,222 | 11,296 | ||||||

|

Securities

available-for-sale

|

124,776 | 108,207 | ||||||

|

Securities

held-to-maturity

|

19,557 | 18,515 | ||||||

|

Loans

held for sale

|

1,025 | – | ||||||

|

Loans

receivable

|

458,245 | 489,509 | ||||||

|

Less:

allowance for loan losses

|

(6,114 | ) | (5,830 | ) | ||||

|

Net

loans receivable

|

452,131 | 483,679 | ||||||

|

Federal

Home Loan Bank stock

|

3,650 | 3,650 | ||||||

|

Accrued

interest receivable

|

2,878 | 3,160 | ||||||

|

Premises

and equipment

|

19,590 | 19,083 | ||||||

|

Foreclosed

real estate

|

3,747 | 527 | ||||||

|

Cash

value of bank owned life insurance

|

12,049 | 11,641 | ||||||

|

Prepaid

FDIC insurance premium

|

3,282 | – | ||||||

|

Other

assets

|

5,899 | 4,974 | ||||||

|

Total

assets

|

$ | 661,806 | $ | 664,732 | ||||

|

LIABILITIES

AND STOCKHOLDERS’ EQUITY

|

||||||||

|

Deposits:

|

||||||||

|

Non-interest

bearing

|

$ | 42,390 | $ | 43,367 | ||||

|

Interest

bearing

|

498,137 | 484,781 | ||||||

|

Total

|

540,527 | 528,148 | ||||||

|

Repurchase

agreements

|

15,893 | 25,773 | ||||||

|

Borrowed

funds

|

47,129 | 49,022 | ||||||

|

Accrued

expenses and other liabilities

|

5,179 | 9,016 | ||||||

|

Total

liabilities

|

608,728 | 611,959 | ||||||

|

Stockholders’

Equity:

|

||||||||

|

Preferred

stock, no par or stated value;

|

||||||||

|

10,000,000

shares authorized, none outstanding

|

– | – | ||||||

|

Common

stock, no par or stated value; 10,000,000 shares

authorized;

|

||||||||

|

shares

issued: December 31, 2009 - 2,889,452

|

||||||||

|

December

31, 2008 - 2,887,452

|

||||||||

|

shares

outstanding: December 31, 2009 - 2,818,578

|

||||||||

|

December 31, 2008 - 2,809,075

|

361 | 361 | ||||||

|

Additional

paid-in capital

|

5,104 | 5,064 | ||||||

|

Accumulated

other comprehensive income/(loss)

|

(170 | ) | (1,289 | ) | ||||

|

Retained

earnings

|

49,312 | 50,365 | ||||||

|

Treasury

stock, common shares at cost: December 31, 2009 - 70,874

|

||||||||

|

December

31, 2008 - 78,377

|

(1,529 | ) | (1,728 | ) | ||||

|

Total

stockholders’ equity

|

53,078 | 52,773 | ||||||

|

Total

liabilities and stockholders’ equity

|

$ | 661,806 | $ | 664,732 | ||||

|

|

Year ended December 31,

|

|||||||

| (Dollars in thousands, except per share data) |

2009

|

2008

|

||||||

|

Interest

income:

|

||||||||

|

Loans

receivable

|

||||||||

|

Real

estate loans

|

$ | 22,046 | $ | 25,274 | ||||

|

Commercial

loans

|

3,822 | 3,843 | ||||||

|

Consumer

loans

|

121 | 152 | ||||||

|

Total

loan interest

|

25,989 | 29,269 | ||||||

|

Securities

|

6,185 | 5,833 | ||||||

|

Other

interest earning assets

|

15 | 65 | ||||||

|

Total

interest income

|

32,189 | 35,167 | ||||||

|

Interest

expense:

|

||||||||

|

Deposits

|

7,083 | 10,648 | ||||||

|

Repurchase

agreements

|

290 | 432 | ||||||

|

Borrowed

funds

|

1,468 | 1,853 | ||||||

|

Total

interest expense

|

8,841 | 12,933 | ||||||

|

Net

interest income

|

23,348 | 22,234 | ||||||

|

Provision

for loan losses

|

8,540 | 2,388 | ||||||

|

Net

interest income after provision for loan losses

|

14,808 | 19,846 | ||||||

|

Noninterest

income:

|

||||||||

|

Fees

and service charges

|

2,661 | 2,898 | ||||||

|

Gain

on sale of loans, net

|

1,139 | 108 | ||||||

|

Wealth

management operations

|

933 | 814 | ||||||

|

Gain

on sales of securities, net

|

736 | 210 | ||||||

|

Increase

in cash value of bank owned life insurance

|

407 | 413 | ||||||

|

Loss

on sale of foreclosed real estate

|

(161 | ) | (52 | ) | ||||

|

Other-than-temporary

credit loss impairment of debt securities

|

(523 | ) | – | |||||

|

Net

credit portion of gain recognized in other comprehensive

income

|

387 | – | ||||||

|

Other

|

23 | 137 | ||||||

|

Total

noninterest income

|

5,602 | 4,528 | ||||||

|

Noninterest

expense:

|

||||||||

|

Compensation

and benefits

|

9,346 | 8,822 | ||||||

|

Occupancy

and equipment

|

2,893 | 2,834 | ||||||

|

Federal

deposit insurance premiums

|

1,227 | 348 | ||||||

|

Data

processing

|

871 | 852 | ||||||

|

Marketing

|

469 | 405 | ||||||

|

Statement

and check processing

|

325 | 378 | ||||||

|

Professional

services

|

261 | 329 | ||||||

|

Other

|

3,343 | 3,031 | ||||||

|

Total

noninterest expense

|

18,735 | 16,999 | ||||||

|

Income

before income tax expenses

|

1,675 | 7,375 | ||||||

|

Income

tax (benefits) expenses

|

(813 | ) | 1,445 | |||||

|

Net

income

|

$ | 2,488 | $ | 5,930 | ||||

|

Earnings

per common share:

|

||||||||

|

Basic

|

$ | 0.88 | $ | 2.11 | ||||

|

Diluted

|

$ | 0.88 | $ | 2.10 | ||||

|

Dividends

declared per common share

|

$ | 1.21 | $ | 1.44 | ||||

|

Accumulated

|

||||||||||||||||||||||||

|

Additional

|

Other

|

|||||||||||||||||||||||

|

Common

|

Paid-in

|

Comprehensive

|

Retained

|

Treasury

|

Total

|

|||||||||||||||||||

|

(Dollars

in thousands, except per share data)

|

Stock

|

Capital

|

Income (Loss)

|

Earnings

|

Stock

|

Equity

|

||||||||||||||||||

|

Balance

at December 31, 2007

|

360 | 4,895 | 563 | 48,500 | (1,585 | ) | 52,733 | |||||||||||||||||

|

Comprehensive

income:

|

||||||||||||||||||||||||

|

Net

income

|

– | – | – | 5,930 | – | 5,930 | ||||||||||||||||||

|

Net

unrealized gain/(loss) on securities available-for-sale, net of

reclassification and tax effects

|

– | – | (1,841 | ) | – | – | (1,841 | ) | ||||||||||||||||

|

Change

in unrecognized gain on post retirement benefit, net of reclassification

and tax effects

|

– | – | (11 | ) | – | – | (11 | ) | ||||||||||||||||

|

Comprehensive

income

|

– | – | – | – | – | 4,078 | ||||||||||||||||||

|

Issuance

of 5,355 shares of common stock at $20.50 - $28.00 per share, under

stock-based compensation plans, including related tax

effects

|

1 | 106 | – | – | – | 107 | ||||||||||||||||||

|

Stock-based

compensation expense

|

– | 57 | – | – | – | 57 | ||||||||||||||||||

|

Purchase

of treasury stock

|

– | – | – | – | (226 | ) | (226 | ) | ||||||||||||||||

|

Sale

of treasury stock

|

– | 6 | – | – | 83 | 89 | ||||||||||||||||||

|

Adjustments

to retained earnings for split-dollar life insurance

arrangements

|

– | – | – | (20 | ) | – | (20 | ) | ||||||||||||||||

|

Cash

dividends, $1.44 per share

|

– | – | – | (4,045 | ) | – | (4,045 | ) | ||||||||||||||||

|

Balance

at December 31, 2008

|

$ | 361 | $ | 5,064 | $ | (1,289 | ) | $ | 50,365 | $ | (1,728 | ) | $ | 52,773 | ||||||||||

|

Comprehensive

income:

|

||||||||||||||||||||||||

|

Net

income

|

– | – | – | 2,488 | – | 2,488 | ||||||||||||||||||

|

Net

unrealized gain/(loss) on securities available-for-sale, net of

reclassification and tax effects

|

– | – | 1,128 | – | – | 1,128 | ||||||||||||||||||

|

Change

in unrecognized gain on post retirement benefit, net of reclassification

and tax effects

|

– | – | (9 | ) | – | – | (9 | ) | ||||||||||||||||

|

Comprehensive

income

|

– | – | – | – | – | 3,607 | ||||||||||||||||||

|

Issuance

of 9,503 shares of common stock at $18.50 - $20.50 per share, under

stock-based compensation plans, including related tax

effects

|

– | 6 | – | – | – | 6 | ||||||||||||||||||

|

Stock-based

compensation expense

|

– | 40 | – | – | – | 40 | ||||||||||||||||||

|

Sale

of treasury stock

|

– | (6 | ) | – | (52 | ) | 199 | 141 | ||||||||||||||||

|

Adjustments

to retained earnings for split-dollar life insurance

arrangements

|

– | – | – | (84 | ) | – | (84 | ) | ||||||||||||||||

|

Cash

dividends, $1.21 per share

|

– | – | – | (3,405 | ) | – | (3,405 | ) | ||||||||||||||||

|

Balance

at December 31, 2009

|

$ | 361 | $ | 5,104 | $ | (170 | ) | $ | 49,312 | $ | (1,529 | ) | $ | 53,078 | ||||||||||

|

Year Ended December 31,

|

||||||||

|

(Dollars in thousands)

|

2009

|

2008

|

||||||

|

CASH

FLOWS FROM OPERATING ACTIVITIES:

|

||||||||

|

Net

income

|

$ | 2,488 | $ | 5,930 | ||||

|

Adjustments

to reconcile net income to net cash provided by operating

activities:

|

||||||||

|

Origination

of loans for sale

|

(49,670 | ) | (4,225 | ) | ||||

|

Sale

of loans originated for sale

|

49,449 | 4,333 | ||||||

|

Depreciation

and amortization, net of accretion

|

1,457 | 1,330 | ||||||

|

Amortization

of mortgage servicing rights

|

144 | 98 | ||||||

|

Amortization

of investment in real estate limited partnerships

|

26 | 32 | ||||||

|

Equity

in loss of investments in real estate limited partnership, net of interest

received

|

151 | 41 | ||||||

|

Stock

based compensation expense

|

40 | 57 | ||||||

|

Net

gains on sales and calls of securities

|

(736 | ) | (210 | ) | ||||

|

Net

gains on sale of loans

|

(1,139 | ) | (108 | ) | ||||

|

Net

losses due to other-than-temporary impairment of

securities

|

136 | – | ||||||

|

Net

losses on foreclosed real estate

|

161 | 52 | ||||||

|

Provision

for loan losses

|

8,540 | 2,388 | ||||||

|

Net

change in:

|

||||||||

|

Interest

receivable

|

282 | 134 | ||||||

|

Other

assets

|

(4,964 | ) | (613 | ) | ||||

|

Cash

value of bank owned life insurance

|

(408 | ) | (412 | ) | ||||

|

Accrued

expenses and other liabilities

|

(4,710 | ) | 3,318 | |||||

|

Total

adjustments

|

(1,241 | ) | 6,215 | |||||

|

Net

cash – operating

activities

|

1,247 | 12,145 | ||||||

|

CASH

FLOWS FROM INVESTING ACTIVITIES:

|

||||||||

|

Proceeds

from maturities and paydowns of securities

available-for-sale

|

21,178 | 26,577 | ||||||

|

Proceeds

from sales of securities available-for-sale

|

29,933 | 11,203 | ||||||

|

Purchase

of securities available-for-sale

|

(64,566 | ) | (52,191 | ) | ||||

|

Purchase

of securities held-to-maturity

|

(3,860 | ) | (2,171 | ) | ||||

|

Proceeds

from maturities and paydowns of securities

held-to-maturity

|

2,790 | 1,991 | ||||||

|

Proceeds

from sale of loans transferred to held-for-sale

|

10,651 | – | ||||||

|

Loan

participations purchased

|

– | (957 | ) | |||||

|

Net

change in loans receivable

|

8,744 | (22,094 | ) | |||||

|

Purchase

of Federal Home Loan Bank Stock

|

– | (100 | ) | |||||

|

Purchase

of premises and equipment, net

|

(1,929 | ) | (4,144 | ) | ||||

|

Proceeds

from sale of foreclosed real estate

|

390 | 372 | ||||||

|

Net

cash – investing

activities

|

3,331 | (41,514 | ) | |||||

|

CASH

FLOWS FROM FINANCING ACTIVITIES:

|

||||||||

|

Change

in deposits

|

12,379 | 34,764 | ||||||

|

Proceeds

from FHLB advances

|

8,000 | 36,000 | ||||||

|

Repayment

of FHLB advances

|

(16,000 | ) | (32,000 | ) | ||||

|

Change

in other borrowed funds

|

(3,773 | ) | (6,135 | ) | ||||

|

Tax

effect of nonqualified stock option exercise

|

– | 6 | ||||||

|

Proceeds

from issuance of common stock

|

6 | 107 | ||||||

|

Proceeds

from sale of treasury stock

|

141 | 83 | ||||||

|

Dividends

paid

|

(3,405 | ) | (4,045 | ) | ||||

|

Treasury

stock purchased

|

– | (226 | ) | |||||

|

Net

cash – financing

activities

|

(2,652 | ) | 28,554 | |||||

|

Net

change in cash and cash equivalents

|

1,926 | (815 | ) | |||||

|

Cash

and cash equivalents at beginning of period

|

11,296 | 12,111 | ||||||

|

Cash

and cash equivalents at end of period

|

$ | 13,222 | $ | 11,296 | ||||

|

SUPPLEMENTAL

CASH FLOW INFORMATION:

|

||||||||

|

Cash

paid during the period for:

|

||||||||

|

Interest

|

$ | 8,947 | $ | 12,916 | ||||

|

Income

taxes

|

$ | 990 | $ | 1,885 | ||||

|

SUPPLEMENTAL

NONCASH INFORMATION:

|

||||||||

|

Transfers

from loans to foreclosed real estate

|

$ | 3,763 | $ | 817 | ||||

|

Transfers

from loans to loans held for sale

|

$ | 10,497 | – | |||||

|

(Dollars in thousands)

|

||||||||||||||||

|

Gross

|

Gross

|

|||||||||||||||

|

Cost

|

Unrealized

|

Unrealized

|

Fair

|

|||||||||||||

|

Basis

|

Gains

|

Losses

|

Value

|

|||||||||||||

|

2009

|

||||||||||||||||

|

U.S.

government sponsored securities

|

$ | 1,993 | $ | 52 | $ | – | $ | 2,045 | ||||||||

|

CMO

and residential mortgage-backed securities

|

61,095 | 2,302 | (82 | ) | 63,315 | |||||||||||

|

Municipal

securities

|

34,151 | 1,516 | (94 | ) | 35,573 | |||||||||||

|

Corporate

debt securities

|

– | – . | – | – | ||||||||||||

|

CMO

government sponsored entities

|

22,534 | 168 | (209 | ) | 22,493 | |||||||||||

|

Collateralized

debt obligations

|

5,343 | – . | (3,993 | ) | 1,350 | |||||||||||

|

Total

debt securities

|

$ | 125,116 | $ | 4,038 | $ | (4,378 | ) | $ | 124,776 | |||||||

|

2008

|

||||||||||||||||

|

U.S.

government sponsored securities

|

$ | 5,484 | $ | 137 | $ | – | $ | 5,621 | ||||||||

|

CMO

and residential mortgage-backed securities

|

63,520 | 1,856 | (7 | ) | 65,369 | |||||||||||

|

Municipal

securities

|

26,952 | 259 | (532 | ) | 26,679 | |||||||||||

|

Corporate

debt securities

|

5,079 | – . | (266 | ) | 4,813 | |||||||||||

|

CMO

government sponsored entities

|

3,756 | 97 | (1 | ) | 3,852 | |||||||||||

|

Collateralized

debt obligations

|

5,481 | – . | (3,608 | ) | 1,873 | |||||||||||

|

Total

debt securities

|

$ | 110,272 | $ | 2,349 | $ | (4,414 | ) | $ | 108,207 | |||||||

|

(Dollars in thousands)

|

||||||||||||||||

|

Gross

|

Gross

|

|||||||||||||||

|

Cost

|

Unrecognized

|

Unrecognized

|

Fair

|

|||||||||||||

|

Basis

|

Gains

|

Losses

|

Value

|

|||||||||||||

|

2009

|

||||||||||||||||

|

Municipal

securities

|

$ | 18,539 | $ | 724 | $ | – | $ | 19,263 | ||||||||

|

Residential

mortgage-backed securities

|

1,018 | 28 | (6 | ) | 1,040 | |||||||||||

|

Total

debt securities

|

$ | 19,557 | $ | 752 | $ | (6 | ) | $ | 20,303 | |||||||

|

2008

|

||||||||||||||||

|

Municipal

securities

|

$ | 18,127 | $ | 117 | $ | (263 | ) | $ | 17,981 | |||||||

|

Residential

mortgage-backed securities

|

388 | 16 | – | 404 | ||||||||||||

|

Total

debt securities

|

$ | 18,515 | $ | 133 | $ | (263 | ) | $ | 18,385 | |||||||

|

(Dollars in thousands)

|

||||||||||||

|

Available-for-sale

|

Held-to-maturity

|

|||||||||||

|

Fair

|

Carrying

|

Fair

|

||||||||||

|

Value

|

Amount

|

Value

|

||||||||||

|

Due

in one year or less

|

$ | 191 | $ | 920 | $ | 921 | ||||||

|

Due

from one to five years

|

4,144 | – | – | |||||||||

|

Due

over five years

|

34,633 | 17,619 | 18,342 | |||||||||

|

CMO

and mortgage-backed securities

|

85,808 | 1,018 | 1,040 | |||||||||

|

Total

|

$ | 124,776 | $ | 19,557 | $ | 20,303 | ||||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Proceeds

|

$ | 29,933 | $ | 11,203 | ||||

|

Gross

gains

|

736 | 214 | ||||||

|

Gross

losses

|

– | (5 | ) | |||||

|

(Dollars in thousands)

|

||||||||||||||||||||||||

|

Less than

|

12 months

|

|||||||||||||||||||||||

|

12

months

|

or

longer

|

Total

|

||||||||||||||||||||||

|

Fair

|

Unrealized

|

Fair

|

Unrealized

|

Fair

|

Unrealized

|

|||||||||||||||||||

|

Value

|

Losses

|

Value

|

Losses

|

Value

|

Losses

|

|||||||||||||||||||

|

2009

|

||||||||||||||||||||||||

|

Description

of Securities:

|

||||||||||||||||||||||||

|

U.S.

government sponsored entities

|

$ | – | $ | – | $ | – | $ | – | $ | – | $ | – | ||||||||||||

|

CMO

and residential mortgage-backed securities

|

15,604 | (297 | ) | 13 | – | 15,617 | (297 | ) | ||||||||||||||||

|

Municipal

securities

|

2,443 | (15 | ) | 1,476 | (79 | ) | 3,919 | (94 | ) | |||||||||||||||

|

Corporate

debt securities

|

– | – | – | – | – | – | ||||||||||||||||||

|

Collateralized

debt obligations

|

– | – | 1,350 | (3,993 | ) | 1,350 | (3,993 | ) | ||||||||||||||||

|

Total

temporarily impaired

|

$ | 18,047 | $ | (312 | ) | $ | 2,839 | $ | (4,072 | ) | $ | 20,886 | $ | (4,384 | ) | |||||||||

|

Number

of securities

|

16 | 7 | 23 | |||||||||||||||||||||

|

(Dollars in thousands)

|

||||||||||||||||||||||||

|

Less than

|

12 months

|

|||||||||||||||||||||||

|

12

months

|

or

longer

|

Total

|

||||||||||||||||||||||

|

Fair

|

Unrealized

|

Fair

|

Unrealized

|

Fair

|

Unrealized

|

|||||||||||||||||||

|

Value

|

Losses

|

Value

|

Losses

|

Value

|

Losses

|

|||||||||||||||||||

|

2008

|

||||||||||||||||||||||||

|

Description

of Securities:

|

||||||||||||||||||||||||

|

U.S.

government sponsored entities

|

$ | – | $ | – | $ | 104 | $ | (1 | ) | $ | 104 | $ | (1 | ) | ||||||||||

|

CMO

and residential mortgage-backed securities

|

1,368 | (3 | ) | 371 | (4 | ) | 1,739 | (7 | ) | |||||||||||||||

|

Municipal

securities

|

25,924 | (795 | ) | – | – | 25,924 | (795 | ) | ||||||||||||||||

|

Corporate

debt securities

|

4,813 | (266 | ) | – | – | 4,813 | (266 | ) | ||||||||||||||||

|

Collateralized

debt obligations

|

1,409 | (2,640 | ) | 464 | (968 | ) | 1,873 | (3,608 | ) | |||||||||||||||

|

Total

temporarily impaired

|

$ | 33,514 | $ | (3,704 | ) | $ | 939 | $ | (973 | ) | $ | 34,453 | $ | (4,677 | ) | |||||||||

|

Number

of securities

|

79 | 6 | 85 | |||||||||||||||||||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Loans

secured by real estate:

|

||||||||

|

Construction

and land development

|

$ | 53,288 | $ | 54,975 | ||||

|

Residential,

including home equity

|

184,730 | 238,638 | ||||||

|

Commercial

real estate and other dwelling

|

141,443 | 130,256 | ||||||

|

Total

loans secured by real estate

|

379,461 | 423,869 | ||||||

|

Consumer

loans

|

1,505 | 1,967 | ||||||

|

Commercial

business

|

63,145 | 49,418 | ||||||

|

Government

and other

|

14,474 | 14,783 | ||||||

|

Subtotal

|

458,585 | 490,037 | ||||||

|

Less:

|

||||||||

|

Net

deferred loan origination fees

|

(285 | ) | (347 | ) | ||||

|

Undisbursed

loan funds

|

(55 | ) | (181 | ) | ||||

|

Loans

receivable

|

$ | 458,245 | $ | 489,509 | ||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Balance

at beginning of period

|

$ | 5,830 | $ | 4,581 | ||||

|

Provision

charged to income

|

8,540 | 2,388 | ||||||

|

Loans

charged-off

|

(8,440 | ) | (1,227 | ) | ||||

|

Recoveries

|

184 | 88 | ||||||

|

Balance

at end of period

|

$ | 6,114 | $ | 5,830 | ||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Loans

past due over 90 days still on accrual

|

$ | 1,491 | $ | 1,476 | ||||

|

Non-accrual

loans

|

17,074 | 10,937 | ||||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Year

end loans with no allocated allowances for loan losses

|

$ | 3,853 | $ | 1,748 | ||||

|

Year

end loans with allocated allowances for loan losses (including troubled

debt restructurings of $7,199 and 0)

|

13,112 | 6,819 | ||||||

|

Total

|

$ | 16,965 | $ | 8,567 | ||||

|

Amount

of the allowance for loan losses allocated

|

$ | 1,179 | $ | 1,683 | ||||

|

Average

of impaired loans during the year

|

12,820 | 7,393 | ||||||

|

Interest

income recognized during impairment

|

– | – | ||||||

|

Cash-basis

interest income recognized

|

– | – | ||||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Mortgage

loan portfolio serviced for FHLMC

|

$ | 51,512 | $ | 43,212 | ||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Servicing

rights:

|

||||||||

|

Beginning

of year

|

$ | 276 | $ | 325 | ||||

|

Additions

|

177 | 49 | ||||||

|

Amortized

to expense

|

(144 | ) | (98 | ) | ||||

|

End

of year

|

$ | 309 | $ | 276 | ||||

|

(Dollars in thousands)

|

||||

|

2010

|

$ | 85 | ||

|

2011

|

72 | |||

|

2012

|

61 | |||

|

2013

|

52 | |||

|

2014

|

39 | |||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Cost:

|

||||||||

|

Land

|

$ | 5,069 | $ | 5,069 | ||||

|

Buildings

and improvements

|

17,939 | 16,821 | ||||||

|

Furniture

and equipment

|

10,194 | 9,383 | ||||||

|

Total

cost

|

33,202 | 31,273 | ||||||

|

Less

accumulated depreciation

|

(13,612 | ) | (12,190 | ) | ||||

|

Premises

and equipment, net

|

$ | 19,590 | $ | 19,083 | ||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Commercial

real estate and other dwelling

|

$ | 1,897 | $ | – | ||||

|

Residential

real estate

|

1,082 | 450 | ||||||

|

Construction

and land development

|

768 | 77 | ||||||

|

Total

|

$ | 3,747 | $ | 527 | ||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Federal:

|

||||||||

|

Current

|

$ | (365 | ) | $ | 1,825 | |||

|

Deferred

|

(134 | ) | (305 | ) | ||||

|

State:

|

||||||||

|

Current

|

6 | – | ||||||

|

Deferred

|

(320 | ) | (75 | ) | ||||

|

Income

tax (benefit) expense

|

$ | (813 | ) | $ | 1,445 | |||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Federal

statutory rate

|

34 | % | 34 | % | ||||

|

Tax

expense at statutory rate

|

$ | 569 | $ | 2,507 | ||||

|

State

tax, net of federal effect

|

(201 | ) | (49 | ) | ||||

|

Tax

exempt income

|

(937 | ) | (686 | ) | ||||

|

Bank

owned life insurance

|

(138 | ) | (140 | ) | ||||

|

Tax

credits

|

(112 | ) | (114 | ) | ||||

|

Reversal

of FIN 48

|

– | (84 | ) | |||||

|

Other

|

6 | 11 | ||||||

|

Total

income tax (benefit) expense

|

$ | (813 | ) | $ | 1,445 | |||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Deferred

tax assets:

|

||||||||

|

Bad

debts

|

$ | 2,404 | $ | 2,276 | ||||

|

Deferred

loan fees

|

112 | 136 | ||||||

|

Deferred

compensation

|

636 | 609 | ||||||

|

Unrealized

depreciation on securities available-for-sale

|

92 | 690 | ||||||

|

Net

operating loss

|

709 | 276 | ||||||

|

Tax

credits

|

269 | 24 | ||||||

|

Nonaccrual

loan interest income

|

79 | 37 | ||||||

|

Restricted

stock awards

|

39 | 73 | ||||||

|

REO

writedowns

|

66 | 19 | ||||||

|

Unqualified

DCP

|

42 | 38 | ||||||

|

Post

retirement benefit

|

65 | 75 | ||||||

|

Other-than-temporary

impairment

|

46 | – | ||||||

|

Other

|

6 | 9 | ||||||

|

Total

deferred tax assets

|

4,565 | 4,262 | ||||||

|

Deferred

tax liabilities:

|

||||||||

|

Depreciation

|

(1,137 | ) | (894 | ) | ||||

|

Prepaids

|

(198 | ) | (196 | ) | ||||

|

Mortgage

servicing rights

|

(121 | ) | (108 | ) | ||||

|

Deferred

stock dividends

|

(115 | ) | (115 | ) | ||||

|

FAS

158 - unrealized gain

|

(56 | ) | (62 | ) | ||||

|

Other

|

(18 | ) | (62 | ) | ||||

|

Total

deferred tax liabilities

|

(1,645 | ) | (1,437 | ) | ||||

|

Valuation

allowance

|

(376 | ) | (143 | ) | ||||

|

Net

deferred tax assets

|

$ | 2,544 | $ | 2,682 | ||||

|

(Dollars in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Balance

at beginning of period

|

$ | – | $ | 47 | ||||

|

Additions

based on tax positions related to the current year

|

– | – | ||||||

|

Additions

for tax positions of prior years

|

– | 37 | ||||||

|

Reductions

for tax positions of prior years

|

– | 84 | ||||||

|

Reductions

due to the statute of limitations

|

– | – | ||||||

|

Settlements

|

– | – | ||||||

|

Balance

at end of period

|

$ | – | $ | – | ||||

|

(Dollars in thousands)

|

||||

|

2010

|

$ | 194,611 | ||

|

2011

|

29,740 | |||

|

2012

|

2,215 | |||

|

2013

|

242 | |||

|

2014

|

51 | |||

|

Total

|

$ | 226,859 | ||

|

(Dollars

in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Fixed rate

advances from the FHLB

|

$ | 33,000 | $ | 41,000 | ||||

|

Putable

advances from the FHLB

|

5,000 | 5,000 | ||||||

|

Line

of credit from the FHLB

|

8,464 | 2,044 | ||||||

|

Other

|

665 | 978 | ||||||

|

Total

|

$ | 47,129 | $ | 49,022 | ||||

|

(Dollars

in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Ending

balance

|

$ | 15,893 | $ | 25,773 | ||||

|

Average

balance during the year

|

21,333 | 16,301 | ||||||

|

Maximum

month-end balance during the year

|

23,451 | 25,773 | ||||||

|

Securities

underlying the agreements at year end:

|

||||||||

|

Carrying

value

|

27,394 | 37,414 | ||||||

|

Fair

value

|

27,394 | 37,414 | ||||||

|

Average

interest rate during the year

|

1.36 | % | 2.65 | % | ||||

|

Average

interest rate at year end

|

1.34 | % | 1.46 | % | ||||

|

(Dollars

in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Fixed

rate advances, maturing January 2010 through December 2013, at rates from

1.97% to 4.03% average rate:2009 - 2.98%; 2008 - 3.40%

|

$ | 33,000 | $ | 41,000 | ||||

|

Putable

advances, maturing February 2013 at a rate of 2.62%, average rate: 2009 -

2.62%; 2008 - 2.62%

|

5,000 | 5,000 | ||||||

|

(Dollars in thousands)

|

||||

|

2010

|

$ | 31,129 | ||

|

2011

|

3,000 | |||

|

2012

|

5,000 | |||

|

2013

|

8,000 | |||

|

Total

|

$ | 47,129 | ||

|

Minimum

|

||||||||||||||||||||||||

|

Required

To Be

|

||||||||||||||||||||||||

|

Well

Capitalized

|

||||||||||||||||||||||||

|

Minimum

Required

|

Under

Prompt

|

|||||||||||||||||||||||

|

for

Capital

|

Corrective

|

|||||||||||||||||||||||

|

Actual

|

Adequacy

Purposes

|

Action

Regulations

|

||||||||||||||||||||||

|

(Dollars

in millions)

|

Amount

|

Ratio

|

Amount

|

Ratio

|

Amount

|

Ratio

|

||||||||||||||||||

|

2009

|

||||||||||||||||||||||||

|

Total

capital to risk-weighted assets

|

$ | 58.7 | 11.5 | % | $ | 40.8 | 8.0 | % | $ | 51.0 | 10.0 | % | ||||||||||||

|

Tier

1 capital to risk-weighted assets

|

$ | 52.6 | 10.3 | % | $ | 20.4 | 4.0 | % | $ | 30.6 | 6.0 | % | ||||||||||||

|

Tier

1 capital to adjusted average assets

|

$ | 52.6 | 7.8 | % | $ | 20.1 | 3.0 | % | $ | 33.5 | 5.0 | % | ||||||||||||

|

2008

|

||||||||||||||||||||||||

|

Total

capital to risk-weighted assets

|

$ | 59.9 | 12.0 | % | $ | 39.9 | 8.0 | % | $ | 50.0 | 10.0 | % | ||||||||||||

|

Tier

1 capital to risk-weighted assets

|

$ | 54.1 | 10.8 | % | $ | 20.0 | 4.0 | % | $ | 29.9 | 6.0 | % | ||||||||||||

|

Tier

1 capital to adjusted average assets

|

$ | 54.1 | 8.2 | % | $ | 20.0 | 3.0 | % | $ | 33.1 | 5.0 | % | ||||||||||||

|

|

||||||||||||||||

|

Weighted

|

||||||||||||||||

|

Weighted

|

Average

|

|||||||||||||||

|

Average

|

Remaining

|

Aggregate

|

||||||||||||||

|

Exercise

|

Contractual

|

Intrinsic

|

||||||||||||||

|

Shares

|

Price

|

Term

|

Value

|

|||||||||||||

|

Outstanding

at beginning of year

|

70,597 | $ | 23.56 | |||||||||||||

|

Granted

|

– | – | ||||||||||||||

|

Exercised

|

(200 | ) | 20.50 | |||||||||||||

|

Forfeited

or expired

|

(4,650 | ) | 21.73 | |||||||||||||

|

Outstanding

at end of year

|

65,747 | $ | 23.69 | 2.2 | $ | – | ||||||||||

|

Vested

or expected to vest

|

65,747 | $ | 23.69 | 2.2 | $ | – | ||||||||||

|

Exercisable

at end of year

|

64,747 | $ | 23.62 | 2.1 | $ | – | ||||||||||

|

2009

|

2008

|

|||||||

|

Risk-free

interest rate

|

– | 3.61% | ||||||

|

Expected

term

|

– |

10.0

years

|

||||||

|

Expected

stock price volatility

|

– | 26.55% | ||||||

|

Dividend

yield

|

– | 5.20% | ||||||

|

|

||||||||

|

Weighted

|

||||||||

|

Average

|

||||||||

|

Grant

Date

|

||||||||

|

Nonvested

Shares

|

Shares

|

Fair

Value

|

||||||

|

Nonvested

at January 1, 2009

|

7,550 | $ | 30.14 | |||||

|

Granted

|

2,500 | 18.95 | ||||||

|

Vested

|

(1,800 | ) | 30.50 | |||||

|

Forfeited

|

(700 | ) | 27.93 | |||||

|

Nonvested

at December 31, 2009

|

7,550 | $ | 26.55 | |||||

|

2009

|

2008

|

|||||||

|

Basic

earnings per common share:

|

||||||||

|

Net

income available to common stockholders

|

$ | 2,487,851 | $ | 5,930,255 | ||||

|

Weighted-average

common shares outstanding

|

2,814,488 | 2,809,176 | ||||||

|

Basic

earnings per common share

|

$ | 0.88 | $ | 2.11 | ||||

|

Diluted

earnings per common share:

|

||||||||

|

Net

income available to common stockholders

|

$ | 2,487,851 | $ | 5,930,255 | ||||

|

Weighted-average

common shares outstanding

|

2,814,488 | 2,809,176 | ||||||

|

Add:

dilutive effect of assumed stock option exercises and restricted

stock

|

– | 16,595 | ||||||

|

Weighted-average

common and dilutive potential common shares outstanding

|

2,814,488 | 2,825,771 | ||||||

|

Diluted

earnings per common share

|

$ | 0.88 | $ | 2.10 | ||||

|

(Dollars in thousands)

|

||||

|

Aggregate

balance - January 1, 2009

|

$ | 8,999 | ||

|

New

loans

|

1,200 | |||

|

Repayments

|

(374 | ) | ||

|

Aggregate

balance - December 31, 2009

|

$ | 9,825 | ||

|

(Dollars

in thousands)

|

||||||||||||

|

Fixed

|

Variable

|

|||||||||||

|

Rate

|

Rate

|

Total

|

||||||||||

|

December

31, 2009:

|

||||||||||||

|

Commercial

business

|

$ | – | $ | 58,493 | $ | 58,493 | ||||||

|

Real

estate

|

5,731 | 21,895 | 27,626 | |||||||||

|

Consumer

loans

|

– | 20 | 20 | |||||||||

|

Unsecured

consumer overdrafts

|

10,751 | – | 10,751 | |||||||||

|

Total

|

$ | 16,482 | $ | 80,408 | $ | 96,890 | ||||||

|

December

31, 2008:

|

||||||||||||

|

Commercial

business

|

$ | – | $ | 42,458 | $ | 42,458 | ||||||

|

Real

estate

|

11,890 | 28,618 | 40,508 | |||||||||

|

Consumer

loans

|

– | 17 | 17 | |||||||||

|

Unsecured

consumer overdrafts

|

12,345 | – | 12,345 | |||||||||

|

Total

|

$ | 24,235 | $ | 71,093 | $ | 95,328 | ||||||

|

(Dollars

in thousands)

|

||||

|

Collateralized

debt

|

||||

|

obligations

other-

|

||||

|

than-temporarily

|

||||

|

impaired

|

||||

|

Ending

balance - December 31, 2008

|

$ | – | ||

|

Additions

not previously recognized

|

136 | |||

|

Ending

balance - December 31, 2009

|

$ | 136 | ||

|

Deal

name

|

PreTSL

XXIV

|

PreTSL

XXVII

|

Alesco

IX

|

Alesco

XVII

|

||||||||||||

|

Class

|

B-1 | C-1 | A-2A | B | ||||||||||||

|

Book

value

|

1,258,772 | 1,409,027 | 1,323,252 | 1,351,903 | ||||||||||||

|

Fair

value

|

250,849 | 263,336 | 646,350 | 189,462 | ||||||||||||

|

Unrealized

gains/(losses)

|

(1,007,922 | ) | (1,145,692 | ) | (676,902 | ) | (1,162,441 | ) | ||||||||

|

Lowest

credit rating assigned

|

Caa3

|

Ca

|

BB

|

Ca

|

||||||||||||

|

Number

of performing banks

|

57 | 30 | 63 | 40 | ||||||||||||

|

Number

of performing insurance companies

|

12 | 7 | 11 | n/a | ||||||||||||

|

Number

of issuers in default

|

9 | 3 | 7 | 6 | ||||||||||||

|

Number

of issuers in deferral

|

15 | 9 | 6 | 10 | ||||||||||||

|

Defaults

& deferrals as a % of performing collateral

|

29.40 | % | 21.20 | % | 28.64 | % | 38.79 | % | ||||||||

|

Subordination:

|

||||||||||||||||

|

As

a % of performing collateral

|

-10.09 | % | -12.77 | % | 22.82 | % | -1.33 | % | ||||||||

|

As

a % of performing collateral - adjusted for projected future

defaults

|

-18.76 | % | -18.95 | % | 14.05 | % | -10.62 | % | ||||||||

|

Other-than-temporary

impairment model assumptions:

|

||||||||||||||||

|

Defaults:

|

||||||||||||||||

|

Year

1 - issuer average

|

5.00 | % | 2.90 | % | 7.20 | % | 5.80 | % | ||||||||

|

Year

2 - issuer average

|

1.70 | % | 1.70 | % | 2.40 | % | 2.10 | % | ||||||||

|

Year

3 - issuer average

|

0.60 | % | 0.60 | % | 0.60 | % | 0.50 | % | ||||||||

|

>

3 Years- issuer average

|

(1 | ) | (1 | ) | (1 | ) | (1 | ) | ||||||||

|

Discount

rate - 3-month LIBOR plus implicit yield spread at

purchase

|

1.48 | % | 1.23 | % | 1.27 | % | 1.44 | % | ||||||||

|

Recovery

assumptions

|

(2 | ) | (2 | ) | (2 | ) | (2 | ) | ||||||||

|

Prepayments

|

0.00 | % | 0.00 | % | 0.00 | % | 0.00 | % | ||||||||

|

Other-than-temporary impairment

|

39,300 | 19,050 | 15,884 | 61,950 | ||||||||||||

|

(Dollars

in thousands)

|

||||||||||||||||

|

Fair

Value Measurements at December 31, 2009 Using

|

||||||||||||||||

|

Quoted

Prices

|

Significant

|

|||||||||||||||

|

in

Active

|

Other

|

Significant

|

||||||||||||||

|

Markets

for

|

Observable

|

Unobservable

|

||||||||||||||

|

December

31,

|

Identical

Assets

|

Inputs

|

Inputs

|

|||||||||||||

|

2009

|

(Level

1)

|

(Level

2)

|

(Level

3)

|

|||||||||||||

|

Assets:

|

||||||||||||||||

|

Available

for sale securities

|

$ | 124,776 | $ | – | $ | 123,426 | $ | 1,350 | ||||||||

|

(Dollars

in thousands)

|

||||||||||||||||

|

Fair

Value Measurements at December 31, 2008 Using

|

||||||||||||||||

|

Quoted

Prices

|

Significant

|

|||||||||||||||

|

in

Active

|

Other

|

Significant

|

||||||||||||||

|

Markets

for

|

Observable

|

Unobservable

|

||||||||||||||

|

December

31,

|

Identical

Assets

|

Inputs

|

Inputs

|

|||||||||||||

|

2008

|

(Level

1)

|

(Level

2)

|

(Level

3)

|

|||||||||||||

|

Assets:

|

||||||||||||||||

|

Available

for sale securities

|

$ | 108,207 | $ | – | $ | 107,204 | $ | 1,003 | ||||||||

|

(Dollars

in thousands)

|

||||

|

Fair

Value Measurements

|

||||

|

Using

Significant

|

||||

|

Unobservable

Inputs

|

||||

|

(Level

3)

|

||||

|

Available

for sale securities

|

||||

|

Beginning

balance - January 1, 2008

|

$ | – | ||

|

Included

in other comprehensive income

|

440 | |||

|

Transfers

in and/or out of Level 3

|

563 | |||

|

Ending

balance - December 31, 2008

|

1,003 | |||

|

Total

realized/unrealized losses

|

||||

|

Included

in earnings

|

(136 | ) | ||

|

Included

in other comprehensive income

|

33 | |||

|

Transfers

in and/or out of Level 3

|

450 | |||

|

Ending

balance - December 31, 2009

|

$ | 1,350 | ||

|

(Dollars

in thousands)

|

||||||||||||||||

|

Fair

Value Measurements at December 31, 2009 Using

|

||||||||||||||||

|

Quoted

Prices

|

Significant

|

|||||||||||||||

|

in

Active

|

Other

|

Significant

|

||||||||||||||

|

Markets

for

|

Observable

|

Unobservable

|

||||||||||||||

|

December

31,

|

Identical

Assets

|

Inputs

|

Inputs

|

|||||||||||||

|

2009

|

(Level

1)

|

(Level

2)

|

(Level

3)

|

|||||||||||||

|

Assets:

|

||||||||||||||||

|

Impaired

loans

|

$ | 11,933 | $ | – | $ | – | $ | 11,933 | ||||||||

|

Foreclosed

real estate

|

3,738 | – | – | 3,738 | ||||||||||||

|

(Dollars

in thousands)

|

||||||||||||||||

|

Fair

Value Measurements at December 31, 2008 Using

|

||||||||||||||||

|

Quoted

Prices

|

Significant

|

|||||||||||||||

|

in

Active

|

Other

|

Significant

|

||||||||||||||

|

Markets

for

|

Observable

|

Unobservable

|

||||||||||||||

|

December

31,

|

Identical

Assets

|

Inputs

|

Inputs

|

|||||||||||||

|

2008

|

(Level

1)

|

(Level

2)

|

(Level

3)

|

|||||||||||||

|

Assets:

|

||||||||||||||||

|

Impaired

loans

|

$ | 5,523 | $ | – | $ | 2,789 | $ | 2,734 | ||||||||

|

Foreclosed

real estate

|

527 | – | – | 527 | ||||||||||||

|

(Dollars

in thousands)

|

||||||||

|

December

31,

2009

|

||||||||

|

Carrying

|

Estimated

|

|||||||

|

Value

|

Fair

Value

|

|||||||

|

Financial

assets

|

||||||||

|

Cash

and cash equivalents

|

$ | 13,222 | $ | 13,222 | ||||

|

Securities

available-for-sale

|

124,776 | 124,776 | ||||||

|

Securities

held-to-maturity

|

19,557 | 20,303 | ||||||

|

Loans

held for sale

|

1,025 | 1,025 | ||||||

|

Loans

receivable, net

|

452,131 | 498,005 | ||||||

|

Federal

Home Loan Bank stock

|

3,650 | 3,650 | ||||||

|

Accrued

interest receivable

|

2,878 | 2,878 | ||||||

|

Financial

liabilities

|

||||||||

|

Demand

and savings deposits

|

313,669 | 313,669 | ||||||

|

Certificates

of deposit

|

226,858 | 227,672 | ||||||

|

Repurchase

agreements

|

15,893 | 15,525 | ||||||

|

Borrowed

funds

|

47,129 | 38,932 | ||||||

|

Accrued

interest payable

|

150 | 150 | ||||||

|

(Dollars

in thousands)

|

||||||||

|

December

31,

2008

|

||||||||

|

Carrying

|

Estimated

|

|||||||

|

Value

|

Fair

Value

|

|||||||

|

Financial

assets

|

||||||||

|

Cash

and cash equivalents

|

$ | 11,296 | $ | 11,296 | ||||

|

Securities

available-for-sale

|

108,207 | 108,207 | ||||||

|

Securities

held-to-maturity

|

18,515 | 18,385 | ||||||

|

Loans

held for sale

|

– | – | ||||||

|

Loans

receivable, net

|

483,679 | 533,377 | ||||||

|

Federal

Home Loan Bank stock

|

3,650 | 3,650 | ||||||

|

Accrued

interest receivable

|

3,160 | 3,160 | ||||||

|

Financial

liabilities

|

||||||||

|

Demand

and savings deposits

|

297,076 | 297,076 | ||||||

|

Certificates

of deposit

|

231,072 | 232,926 | ||||||

|

Repurchase

agreements

|

25,773 | 25,464 | ||||||

|

Borrowed

funds

|

49,022 | 49,702 | ||||||

|

Accrued

interest payable

|

256 | 256 | ||||||

|

(Dollars

in thousands)

|

||||||||

|

2009

|

2008

|

|||||||

|

Net

change in net unrealized gains and losses

on securities available for sale:

|

||||||||

|

Unrealized

gains/(losses) arising during

the year

|

$ | 1,125 | $ | (2,981 | ) | |||

|

Reclassification

adjustment for gains included

in net income

|

600 | 210 | ||||||

|

Net

securities gain/(loss) during the year

|

1,725 | (2,771 | ) | |||||

|

Tax

effect

|

(597 | ) | 930 | |||||

|

Net

of tax amount

|

1,128 | (1,841 | ) | |||||

|

Net

change in unrecognized gain on post

retirement benefit:

|

||||||||

|

Net

gain/(loss) on post retirement benefit

|

6 | 5 | ||||||

|

Amortization

of net actuarial gain

|

(15 | ) | (16 | ) | ||||

|

Net

gain/(loss) activity during the year

|

(9 | ) | (11 | ) | ||||

|

Tax

effect

|

– | – | ||||||

|

Net

of tax amount

|

(9 | ) | (11 | ) | ||||

|

Other

comprehensive income (loss), net of tax

|

$ | 1,119 | $ | (1,852 | ) | |||

|

(Dollars

in thousands)

|

||||||||||||

|

Balance

at

|

Current

|

Balance

at

|

||||||||||

|

December

31,

|

Period

|

December

31,

|

||||||||||

|

2008

|

Change

|

2009

|

||||||||||

|

Unrealized

gains (losses) on securities available for

sale

|

$ | (1,375 | ) | $ | 1,128 | $ | (247 | ) | ||||

|

Unrealized

gain (loss) on pension benefits

|

86 | (9 | ) | 77 | ||||||||

|

Total

|

$ | (1,289 | ) | $ | 1,119 | $ | (170 | ) | ||||

|

(Dollars

in thousands)

|

||||||||

|

NorthWest

Indiana Bancorp

|

||||||||

|

Condensed

Balance Sheets

|

||||||||

|

December

31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Assets

|

||||||||

|

Cash

on deposit with Peoples Bank

|

$ | 2,691 | $ | 1,867 | ||||

|

Investment

in Peoples Bank

|

52,212 | 51,384 | ||||||

|

Dividends

receivable from Peoples Bank

|

– | 1,012 | ||||||

|

Other

assets

|

107 | 219 | ||||||

|

Total

assets

|

$ | 55,010 | $ | 54,482 | ||||

|

Liabilities

and stockholders’ equity

|

||||||||

|

Dividends

payable

|

$ | 594 | $ | 1,011 | ||||

|

Other

liabilities

|

1,338 | 698 | ||||||

|

Total

liabilities

|

1,932 | 1,709 | ||||||

|

Common

stock

|

361 | 361 | ||||||

|

Additional

paid in capital

|

5,104 | 5,064 | ||||||

|

Accumulated

other comprehensive income (loss)

|

(170 | ) | (1,289 | ) | ||||

|

Retained

earnings

|

49,312 | 50,365 | ||||||

|

Treasury

stock

|

(1,529 | ) | (1,728 | ) | ||||

|

Total

stockholders’ equity

|

53,078 | 52,773 | ||||||

|

Total

liabilities and stockholders’ equity

|

$ | 55,010 | $ | 54,482 | ||||

|

(Dollars

in thousands)

|

||||||||

|

NorthWest

Indiana Bancorp

|

||||||||

|

Condensed

Statements of Income

|

||||||||

|

Year

Ended December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Dividends

from Peoples Bank

|

$ | 2,813 | $ | 4,047 | ||||

|

Operating

expenses

|

176 | 161 | ||||||

|

Income

before income taxes and equity in undistributed income of Peoples

Bank

|

2,637 | 3,886 | ||||||

|

Income

tax benefit

|

(58 | ) | (61 | ) | ||||

|

Income

before equity in undistributed income of Peoples Bank

|

2,695 | 3,947 | ||||||

|

Equity/(loss)

in undistributed income of Peoples Bank

|

(207 | ) | 1,983 | |||||

|

Net

income

|

$ | 2,488 | $ | 5,930 | ||||

|

(Dollars

in thousands)

|

||||||||

|

NorthWest

Indiana Bancorp

|

||||||||

|

Condensed

Statements of Cash Flows

|

||||||||

|

Year

Ended December 31,

|

||||||||

|

2009

|

2008

|

|||||||

|

Cash

flows from operating activities:

|

||||||||

|

Net

income

|

$ | 2,488 | $ | 5,930 | ||||

|

Adjustments

to reconcile net income to net cash from operating

activities

|

||||||||

|

Equity

in undistributed net income of Peoples Bank

|

207 | (1,983 | ) | |||||

|

Stock-based

compensation expense

|

40 | 57 | ||||||

|

Change

in other assets

|

1,123 | 33 | ||||||

|

Change

in other liabilities

|

224 | 151 | ||||||

|

Total

adjustments

|

1,594 | (1,742 | ) | |||||

|

Net

cash from operating activities

|

4,082 | 4,188 | ||||||

|

Cash

flows from investing activities

|

– | – | ||||||

|

Cash

flows from financing activities:

|

||||||||

|

Dividends

paid

|

(3,405 | ) | (4,045 | ) | ||||

|

Treasury

stock purchased

|

– | (226 | ) | |||||

|

Sale

of treasury stock

|

141 | 83 | ||||||

|

Proceeds

from issuance of common stock

|

6 | 113 | ||||||

|

Net

cash used in financing activities

|

(3,258 | ) | (4,075 | ) | ||||

|

Net

change in cash

|

824 | 113 | ||||||

|

Cash

at beginning of year

|

1,867 | 1,754 | ||||||

|

Cash

at end of year

|

$ | 2,691 | $ | 1,867 | ||||

|

Dividends

|

|||||||||||||

|

Per

Share Prices

|

Declared

Per

|

||||||||||||

|

High

|

Low

|

Common

Share

|

|||||||||||

| Year Ended | |||||||||||||

|

December

31, 2009

|

1st

Quarter

|

$ | 24.00 | $ | 16.00 | $ | 0.36 | ||||||

|

|

2nd

Quarter

|

20.00 | 18.25 | 0.32 | |||||||||

|

3rd

Quarter

|

20.50 | 17.00 | 0.32 | ||||||||||

|

4th

Quarter

|

19.95 | 17.25 | 0.21 | ||||||||||

|

Year

Ended

|

|||||||||||||

|

December

31, 2008

|

1st

Quarter

|

$ | 29.90 | $ | 23.10 | $ | 0.36 | ||||||

|

|

2nd

Quarter

|

27.25 | 26.00 | 0.36 | |||||||||

|

3rd

Quarter

|

29.00 | 26.00 | 0.36 | ||||||||||

|

4th

Quarter

|

27.25 | 24.00 | 0.36 | ||||||||||