2010 Annual Report

|

|

| |

|

David A. Bochnowski

Chairman and

Chief Executive Officer

|

Dear Shareholder,

2010 was an exciting and at the same time challenging year for the NorthWest Indiana Bancorp: exciting because we celebrated the 100th year of our tradition of community banking; and challenging because of the continuing effects of the Great Recession that has gripped our nation’s economy. On behalf of your Board of Directors and our entire team of dedicated employees, I am pleased to report to you the results of our operations during the last year.

2010 Earnings Double Over the Prior Year

With a strong management team, dedicated community bank employees, strong core earnings, capital, and efficient banking operations, the Bancorp continues to generate operating profits that outpace industry performance.

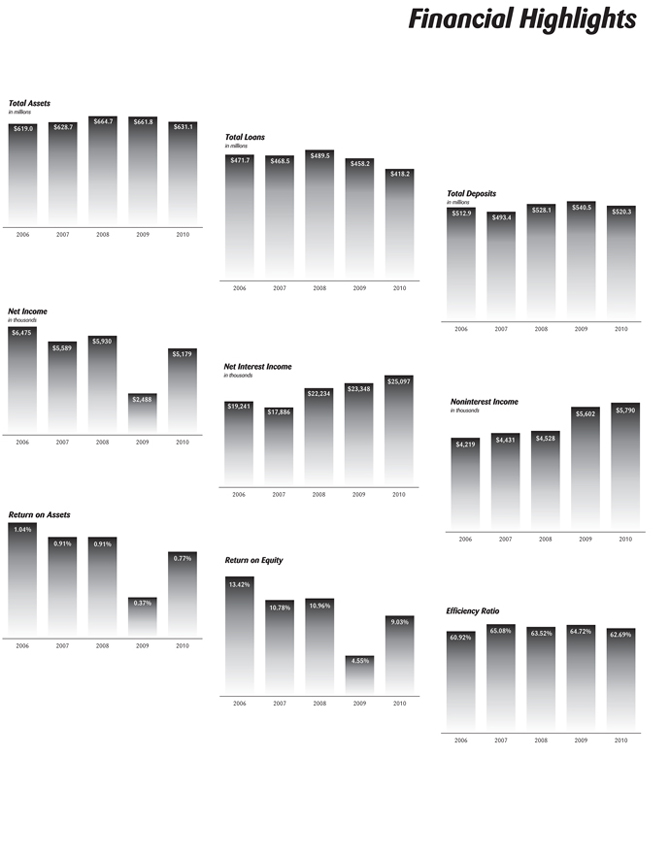

Despite the worst recession in modern times, the Bancorp reported income of $5.2 million in 2010, a 108.2% increase over the prior year. In the midst of this economically challenged environment, we continue to pay dividends and build shareholder value.

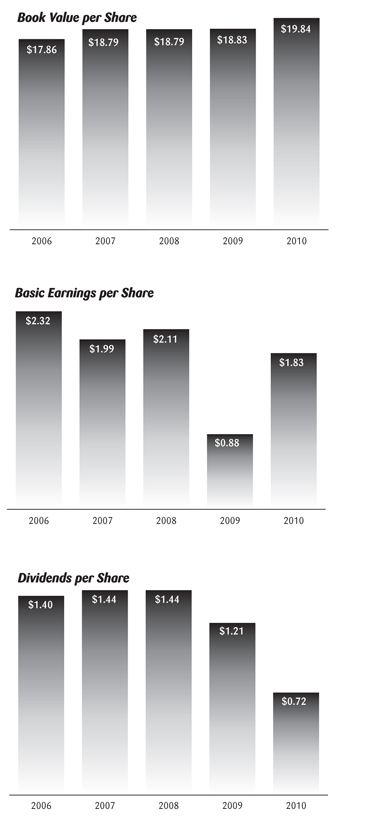

Our key financial ratios proved superior to our community banking peers with our return on assets at 0.77% and our return on equity at 9.03%. The Bancorp’s earnings per share were $1.83 for the year which was also more than twice the $0.88 reported for 2009. Again in 2010, US Banker magazine recognized the Bancorp as one of the Top 200 Community Banks in America.

100 Years Strong

Since 1910, Peoples Bank, our operating subsidiary, has been honored to serve the residents and businesses of Northwest Indiana. From our humble beginnings a century ago, the Bank has grown in stature and reputation to play a major role in the communities we serve. The Bank has weathered many economic storms throughout our history and each time has emerged stronger than before.

The solid values and culture that form the cornerstone of the Bank have remained steadfast for over four generations. Fair and honest dealings have been critical to the success of the enterprise along with an unwavering commitment to consumer and small business needs in our communities. As a result, we have enjoyed the good will and loyalty of our customers, neighbors, community leaders and businesses in Lake and Porter counties.

Economy and Operating Environment

Nationally, signs that the Great Recession was waning began to emerge in the latter part of the year, but unemployment remained stubbornly high. Likewise, consumer confidence showed signs of improvement but households and small businesses continued to close their wallets to new spending and business expansion. Asset values for home and commercial real estate remained in decline as deleveraging impacted the balance sheets of individuals and corporations.

The local economy remained in the doldrums, although promising signs of future activity were seen in rising steel production, modest improvement in employment, and an increase in the number of mortgages tied to first time home buyers as well as empty nester home sales. The Bank’s consumer, home mortgage, and commercial loan officers diligently pursued credit worthy borrowers but were hampered in their endeavors by a lack of consumer confidence in today’s economy. One bright spot in our effort was a modest refinancing boom by home owners who took advantage of low interest rates to reduce their monthly mortgage payments.

In the wake of the stress of the world wide economic slowdown, bank supervisors both in America and abroad signaled the coming of new capital standards for the world’s banking system. The proposed standards require banks, including our nation’s community banks, to hold more capital on their balance sheets as an offset to economic fluctuations. Your company took a proactive stance to these coming changes by taking prudent action to increase capital.

Performance Strategy

The Bancorp’s superior operating results reflect the underlying strength of the Bancorp’s financial and operating performance. The Bank has strong management dedicated to building shareholder, stakeholder, and community value through the utilization of key banking principles.

Our performance has been driven by banking fundamentals and focuses on maintaining strong core earnings, a strong capital position, asset quality, operating efficiency, diversified sources of income from banking operations, and smart growth. We prudently manage the resources entrusted to us by our customers with an outcome that provides sustainable earnings that fund our operations, permit capital growth, and establish reserves for troubled assets in these challenging times.

Core Earnings

The Bank’s operating strategy centers on our net interest margin, the difference between interest earned on loans and investments and payments on deposits and borrowings. For 2010, this measure of core earnings on a tax equivalent basis averaged 4.25%, a remarkable result of our core funding strategy. The Bank continues to be strategically positioned with core funding as the driver of profitability.

We define core accounts as savings, checking, and money market accounts and these three measures combine to provide 61.9% of our total deposit base. At the same time we continue to avoid dependence on non-core funding products like high rate certificates of deposit, deposits brokered through Wall Street investment bankers, and significant borrowings in our liability base.

Although management does not rely on predictions regarding the direction of interest rates, many experts have noted that the current low interest rate policy designed to stimulate the economy cannot be sustained over the longer term. Current monetary policy has driven home loan rates to historic lows with risk to bank earnings should those low rate loans remain on the books when interest rates begin to rise. To mitigate this risk, the Bank sold $41.4 million of fixed rate home mortgage loans into the secondary mortgage market during 2010.

Capital

The Bancorp and our operating subsidiary, Peoples Bank, continue to be well capitalized under applicable federal banking regulations. Our capital strength exceeds all regulatory requirements with the Bancorp’s and Bank’s Tier 1 capital ratio at 8.5% and Total Risk Based Capital for the Bancorp at 12.9% with the Bank’s Total Risk Based Capital at 12.8% at the end of 2010.

During the year, balance sheet strategies were utilized to strengthen our capital ratios through the prudent sale of loans and investments. Our asset base was reduced without damaging our net interest margin as excess liquidity migrated from our balance sheet. In addition, the Board of Directors reduced our dividend to build our capital and preserve the long term capital strength of your company in a changing environment that demands higher levels of capital.

Asset Quality

Asset quality on loans originated by the Bank remained relatively stable throughout the year despite the high unemployment in our primary market territory. Overall, non-performing loans totaled $24.1 million at year end compared to $18.6 million at the end of 2009. The Bank’s non-performing loans are primarily concentrated in five geographically diverse commercial real estate participation loans purchased from other originators prior to the current recession in the period from 2005 through 2007.

The weakness in loan participations does not reflect systemic weakness in our total loans. The Bank’s loan portfolio is well diversified with loan participations comprising only 6.9% of total loans. Management constantly reviews the value of the underlying asset of each participation, utilizing current appraisals to determine current value of each credit facility, the cash flows from each enterprise, and the value added through personal guarantees and financial support of the borrower.

Reserves for potential losses on our loan portfolio are held in our Allowance for Loan Losses (ALL). At year-end, the ALL to total loans was 2.18% compared to 1.33% at the end of 2009. Provisions to the ALL for 2010 were $5.6 million compared to $8.5 million in the prior year. Charge-offs net of recoveries were $2.6 million in 2010 compared to $7.1 million in 2009. The ALL includes $2.8 million of specific reserves for collateral deficiencies, including those associated with the Bank’s participation loans. Management believes that the Bank is adequately reserved for potential losses in our loan portfolio including our participation loans.

Operating Efficiency

Like our shareholders, management recognizes the need to keep tight control on spending especially in the current economy. A key indicator of cost control is measured by a bank’s efficiency ratio, a percentage found by dividing total expenses by all sources of income. Many analysts concur that for a bank our size a ratio near 60% indicates strong cost control. For 2010, the Bancorp reported an efficiency ratio of 62.6% compared to the 64.7% reported last year, with the decline reflecting enhanced cost control and a superior position to 2009.

Banking Operations

Income from banking operations including Wealth Management, the sale of loans, and gains taken on investments provide a valuable source of income that contributes to our bottom line. Our Wealth Management Group’s growing reputation for personal service and investment performance has resulted in increased penetration of its target market with positive results. Assets under management at year-end totaled $238.5 million, an increase of $15.8 million over the prior year. As a result, Wealth Management income for the year totaled $1.2 million, an increase of 24.9% over the prior year.

Opportunities for gain on the sale of loans and investments were also taken advantage of during the year. Income from loan sales totaled $1.3 million, an increase of 10.9% over the prior year. These sales had the effect of decreasing the Bank’s exposure to interest rate risk as long term fixed rate loans were taken off our balance sheet. The sale of investment securities totaled $913 thousand, an increase of 24.1% over the prior year. These transactions enabled the Bank to manage cash flows from securities to shorten portfolio duration, reduce exposure to interest rate risk, and strengthen the Bank’s capital position.

Banking on Our Future

At the beginning of 2011, the Bank entered into the one hundred and first year of our tradition of community banking. We have succeeded for more than a century because of the culture of prudent banking that has endured through four generations of the Bank’s directors, senior managers and team members. We will continue to serve our customers with our commitment to putting customers first with our unique brand of “You First Banking” that has garnered a faithful consumer and small business customer base.

The Bank plans to continue to extend our footprint throughout our trade territory with additional offices. We learn each day that it becomes more and more important to know our customers and understand how and where they want to do their banking. Continuing to know our customers on a personal level is important for two reasons: customer demand shapes our product and service offerings; and in this age of technology, that knowledge helps to foster effective interactive communication.

By understanding how, when, and where our customers want to manage their money and their financial needs, we look to ways to structure and design our product and service lines to complement their behaviors and changing life styles. The Bank has and will continue to anticipate and respond to the on-going shift in consumer preferences as demonstrated by our dynamic menu of electronic banking services, You First checking with customizing features to choose from, or our online behavior-based e-Vantage checking account for paperless checking that appeals to a growing base of technology-driven customers.

Banking behaviors continue to move beyond traditional bricks and mortar and your company intends to be well positioned to continue to deliver products and services that are relevant and meet customer needs. This is the essence of You First Banking that has endured for more than 100 years.

Just as banking preferences have transformed over the last century, the ways in which information is received continues to change. In order to reach out to our customers and stay connected, we continue to evaluate our current methods of communication for effectiveness. Recognizing that the popularity and usage of electronic communication has taken off so dramatically, we continue to explore different outlets of communication including social media, email, and text alerts.

As the Bank continues to grow, our efforts will remain focused on building value for our shareholders and community. Whether our outreach is through new locations or electronic banking, we will continue to stay true to our long standing belief that banking is driven by relationships and not just transactions.

On behalf of the Bancorp’s directors, management and team of dedicated employees, allow me to express my sincere thanks for the relationship we have with you…our shareholders. Despite the fact that in the current business cycle the financial markets have not reflected the soundness of our performance, you have stood with us through the challenges of the current economy and have not wavered from your steadfast support for the Bancorp. Your company pledges to utilize the strong earnings of this year as a platform to continue to build long term shareholder value.

If you have any questions about the Bancorp, please feel free to contact me at 219-853-7575 or by email at dbochnowski@ibankpeoples.com.

| |

Sincerely,

|

| |

|

| |

|

| |

David A. Bochnowski

|

| |

Chairman and Chief Executive Officer

|

Selected Consolidated Financial Data

in thousands of dollars, except per share data

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

|

|

2010

|

|

|

2009

|

|

|

2008

|

|

|

2007

|

|

|

2006

|

|

|

2005

|

|

|

Statement of Income:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total interest income

|

|

$

|

30,086

|

|

|

$

|

32,189

|

|

|

$

|

35,167

|

|

|

$

|

35,768

|

|

|

$

|

34,979

|

|

|

$

|

30,024

|

|

|

Total interest expense

|

|

|

4,989

|

|

|

|

8,841

|

|

|

|

12,933

|

|

|

|

17,882

|

|

|

|

15,738

|

|

|

|

9,758

|

|

|

Net interest income

|

|

|

25,097

|

|

|

|

23,348

|

|

|

|

22,234

|

|

|

|

17,886

|

|

|

|

19,241

|

|

|

|

20,266

|

|

|

Provision for loan losses

|

|

|

5,570

|

|

|

|

8,540

|

|

|

|

2,388

|

|

|

|

552

|

|

|

|

15

|

|

|

|

245

|

|

|

Net interest income after

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

provision for loan losses

|

|

|

19,527

|

|

|

|

14,808

|

|

|

|

19,846

|

|

|

|

17,334

|

|

|

|

19,226

|

|

|

|

20,021

|

|

|

Noninterest income

|

|

|

5,790

|

|

|

|

5,602

|

|

|

|

4,528

|

|

|

|

4,431

|

|

|

|

4,219

|

|

|

|

3,540

|

|

|

Noninterest expense

|

|

|

19,341

|

|

|

|

18,735

|

|

|

|

16,999

|

|

|

|

14,525

|

|

|

|

14,296

|

|

|

|

13,771

|

|

|

Net noninterest expense

|

|

|

13,551

|

|

|

|

13,133

|

|

|

|

12,471

|

|

|

|

10,094

|

|

|

|

10,077

|

|

|

|

10,231

|

|

|

Income tax expenses/(benefit)

|

|

|

797

|

|

|

|

(813

|

)

|

|

|

1,445

|

|

|

|

1,651

|

|

|

|

2,674

|

|

|

|

3,118

|

|

|

Net income

|

|

$

|

5,179

|

|

|

$

|

2,488

|

|

|

$

|

5,930

|

|

|

$

|

5,589

|

|

|

$

|

6,475

|

|

|

$

|

6,672

|

|

|

Basic earnings

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

per common share

|

|

$

|

1.83

|

|

|

$

|

0.88

|

|

|

$

|

2.11

|

|

|

$

|

1.99

|

|

|

$

|

2.32

|

|

|

$

|

2.40

|

|

|

Diluted earnings

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

per common share

|

|

$

|

1.83

|

|

|

$

|

0.88

|

|

|

$

|

2.10

|

|

|

$

|

1.98

|

|

|

$

|

2.30

|

|

|

$

|

2.37

|

|

|

Cash dividends declared

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

per common share

|

|

$

|

0.72

|

|

|

$

|

1.21

|

|

|

$

|

1.44

|

|

|

$

|

1.44

|

|

|

$

|

1.40

|

|

|

$

|

1.32

|

|

| |

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

| |

|

2010

|

|

|

2009

|

|

|

2008

|

|

|

2007

|

|

|

2006

|

|

|

2005

|

|

|

Balance Sheet:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets

|

|

$

|

631,053

|

|

|

$

|

661,806

|

|

|

$

|

664,732

|

|

|

$

|

628,718

|

|

|

$

|

618,982

|

|

|

$

|

627,439

|

|

|

Loans receivable

|

|

|

418,233

|

|

|

|

458,245

|

|

|

|

489,509

|

|

|

|

468,459

|

|

|

|

471,716

|

|

|

|

469,043

|

|

|

Investment securities

|

|

|

160,452

|

|

|

|

144,333

|

|

|

|

126,722

|

|

|

|

114,644

|

|

|

|

99,012

|

|

|

|

90,093

|

|

|

Deposits

|

|

|

520,271

|

|

|

|

540,527

|

|

|

|

528,148

|

|

|

|

493,384

|

|

|

|

512,931

|

|

|

|

525,731

|

|

|

Borrowed funds

|

|

|

48,618

|

|

|

|

63,022

|

|

|

|

74,795

|

|

|

|

76,930

|

|

|

|

51,501

|

|

|

|

51,152

|

|

|

Total stockholders’ equity

|

|

|

56,089

|

|

|

|

53,078

|

|

|

|

52,773

|

|

|

|

52,733

|

|

|

|

50,010

|

|

|

|

46,433

|

|

| |

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

| |

|

2010

|

|

|

2009

|

|

|

2008

|

|

|

2007

|

|

|

2006

|

|

|

2005

|

|

|

Interest Rate Spread During Period:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Average effective yield on loans

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and investment securities

|

|

|

4.84 |

% |

|

|

5.16 |

% |

|

|

5.78 |

% |

|

|

6.21 |

% |

|

|

6.02 |

% |

|

|

5.50 |

% |

|

Average effective cost of deposits

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

and borrowings

|

|

|

0.82 |

% |

|

|

1.45 |

% |

|

|

2.19 |

% |

|

|

3.18 |

% |

|

|

2.77 |

% |

|

|

1.82 |

% |

|

Interest rate spread

|

|

|

4.02 |

% |

|

|

3.71 |

% |

|

|

3.59 |

% |

|

|

3.03 |

% |

|

|

3.25 |

% |

|

|

3.68 |

% |

|

Net interest margin

|

|

|

4.04 |

% |

|

|

3.74 |

% |

|

|

3.65 |

% |

|

|

3.10 |

% |

|

|

3.31 |

% |

|

|

3.71 |

% |

|

Return on average assets

|

|

|

0.77 |

% |

|

|

0.37 |

% |

|

|

0.91 |

% |

|

|

0.91 |

% |

|

|

1.04 |

% |

|

|

1.14 |

% |

|

Return on average equity

|

|

|

9.03 |

% |

|

|

4.55 |

% |

|

|

10.96 |

% |

|

|

10.78 |

% |

|

|

13.42 |

% |

|

|

14.67 |

% |

| |

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

| |

|

2010

|

|

|

2009

|

|

|

2008

|

|

|

2007

|

|

|

2006

|

|

|

2005

|

|

|

Total capital to risk-weighted assets

|

|

|

12.9 |

% |

|

|

11.5 |

% |

|

|

12.0 |

% |

|

|

12.0 |

% |

|

|

12.0 |

% |

|

|

11.6 |

% |

|

Tier 1 capital to risk-weighted assets

|

|

|

11.7 |

% |

|

|

10.3 |

% |

|

|

10.8 |

% |

|

|

11.0 |

% |

|

|

11.1 |

% |

|

|

10.7 |

% |

|

Tier 1 capital to adjusted average assets

|

|

|

8.5 |

% |

|

|

7.8 |

% |

|

|

8.2 |

% |

|

|

8.3 |

% |

|

|

8.0 |

% |

|

|

7.9 |

% |

|

Allowance for loan losses to total loans

|

|

|

2.18 |

% |

|

|

1.33 |

% |

|

|

1.19 |

% |

|

|

0.98 |

% |

|

|

0.90 |

% |

|

|

0.89 |

% |

|

Allowance for loan losses to non-performing loans

|

|

|

42.26 |

% |

|

|

32.93 |

% |

|

|

46.97 |

% |

|

|

53.16 |

% |

|

|

153.95 |

% |

|

|

198.00 |

% |

|

Non-performing loans to total loans

|

|

|

5.77 |

% |

|

|

4.05 |

% |

|

|

2.54 |

% |

|

|

1.84 |

% |

|

|

0.58 |

% |

|

|

0.45 |

% |

|

Total loan accounts

|

|

|

4,594 |

|

|

|

4,846 |

|

|

|

5,193 |

|

|

|

5,268 |

|

|

|

5,392 |

|

|

|

5,422 |

|

|

Total deposit accounts

|

|

|

28,912 |

|

|

|

32,616 |

|

|

|

33,692 |

|

|

|

30,760 |

|

|

|

32,435 |

|

|

|

33,963 |

|

|

Total Banking Centers (all full service)

|

|

|

12 |

|

|

|

11 |

|

|

|

10 |

|

|

|

9 |

|

|

|

8 |

|

|

|

8 |

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

2004

|

|

|

2003

|

|

|

2002

|

|

|

2001

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

$

|

26,614

|

|

|

$

|

26,357

|

|

|

$

|

27,781

|

|

|

$

|

28,425

|

|

| |

6,858

|

|

|

|

7,521

|

|

|

|

10,107

|

|

|

|

13,222

|

|

| |

19,756

|

|

|

|

18,836

|

|

|

|

17,674

|

|

|

|

15,203

|

|

| |

385

|

|

|

|

420

|

|

|

|

720

|

|

|

|

230

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

19,371

|

|

|

|

18,416

|

|

|

|

16,954

|

|

|

|

14,973

|

|

| |

3,312

|

|

|

|

2,968

|

|

|

|

2,675

|

|

|

|

2,402

|

|

| |

13,174

|

|

|

|

12,037

|

|

|

|

10,859

|

|

|

|

9,911

|

|

| |

9,862

|

|

|

|

9,069

|

|

|

|

8,184

|

|

|

|

7,509

|

|

| |

3,219

|

|

|

|

3,411

|

|

|

|

3,277

|

|

|

|

2,754

|

|

|

$

|

6,290

|

|

|

$

|

5,936

|

|

|

$

|

5,493

|

|

|

$

|

4,710

|

|

|

$

|

2.28

|

|

|

$

|

2.16

|

|

|

$

|

2.01

|

|

|

$

|

1.73

|

|

|

$

|

2.24

|

|

|

$

|

2.13

|

|

|

$

|

1.99

|

|

|

$

|

1.71

|

|

|

$

|

1.24

|

|

|

$

|

1.20

|

|

|

$

|

1.12

|

|

|

$

|

1.04

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

2004

|

|

|

2003

|

|

|

2002

|

|

|

2001

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

$

|

557,393

|

|

|

$

|

508,775

|

|

|

$

|

488,002

|

|

|

$

|

440,710

|

|

| |

433,790

|

|

|

|

409,808

|

|

|

|

380,428

|

|

|

|

342,642

|

|

| |

79,979

|

|

|

|

63,733

|

|

|

|

56,571

|

|

|

|

67,260

|

|

| |

451,573

|

|

|

|

421,640

|

|

|

|

406,673

|

|

|

|

355,215

|

|

| |

57,201

|

|

|

|

40,895

|

|

|

|

36,065

|

|

|

|

44,989

|

|

| |

44,097

|

|

|

|

41,554

|

|

|

|

39,148

|

|

|

|

35,882

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

2004

|

|

|

2003

|

|

|

2002

|

|

|

2001

|

|

| |

|

|

|

|

|

|

|

|

|

|

| |

5.31

|

%

|

|

|

5.65

|

%

|

|

|

6.26

|

%

|

|

|

7.29

|

%

|

| |

1.40

|

%

|

|

|

1.67

|

%

|

|

|

2.38

|

%

|

|

|

3.55

|

%

|

| |

3.91

|

%

|

|

|

3.98

|

%

|

|

|

3.88

|

%

|

|

|

3.74

|

%

|

| |

3.94

|

%

|

|

|

4.04

|

%

|

|

|

3.99

|

%

|

|

|

3.90

|

%

|

| |

1.17

|

%

|

|

|

1.20

|

%

|

|

|

1.18

|

%

|

|

|

1.15

|

%

|

| |

14.64

|

%

|

|

|

14.65

|

%

|

|

|

14.58

|

%

|

|

|

13.49

|

%

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

December 31,

|

|

|

2004

|

|

|

2003

|

|

|

2002

|

|

|

2001

|

|

| |

12.2

|

%

|

|

|

12.5

|

%

|

|

|

13.1

|

%

|

|

|

13.6

|

%

|

| |

11.2

|

%

|

|

|

11.5

|

%

|

|

|

11.9

|

%

|

|

|

12.5

|

%

|

| |

8.0

|

%

|

|

|

8.0

|

%

|

|

|

7.6

|

%

|

|

|

8.3

|

%

|

| |

0.90

|

%

|

|

|

0.92

|

%

|

|

|

0.96

|

%

|

|

|

0.92

|

%

|

| |

371.00

|

%

|

|

|

220.31

|

%

|

|

|

152.43

|

%

|

|

|

108.64

|

%

|

| |

0.24

|

%

|

|

|

0.42

|

%

|

|

|

0.63

|

%

|

|

|

0.85

|

%

|

| |

5,370

|

|

|

|

5,213

|

|

|

|

5,049

|

|

|

|

4,964

|

|

| |

32,866

|

|

|

|

32,502

|

|

|

|

31,385

|

|

|

|

30,433

|

|

| |

8

|

|

|

|

8

|

|

|

|

8

|

|

|

|

8

|

|

Business

NorthWest Indiana Bancorp (the Bancorp) is a bank holding company registered with the Board of Governors of the Federal Reserve System. Peoples Bank (the Bank), an Indiana bank, is a wholly owned subsidiary of the Bancorp. The Bancorp has no other business activity other than being the holding company for the Bank.

The Bancorp conducts business from its Corporate Center in Munster and its twelve full-service offices located in Crown Point, Dyer, East Chicago, Gary, Hammond, Hobart, Merrillville, Munster, St. John, Schererville, and Valparaiso, Indiana. The Bancorp is primarily engaged in the business of attracting deposits from the general public and the origination of loans secured by single family residences and commercial real estate, as well as, construction loans, various types of consumer loans and commercial business loans, and loans to local municipalities. In addition, the Bancorp's Wealth Management Group provides estate and retirement planning, guardianships, land trusts, profit sharing and 401(k) retirement plans,

IRA and Keogh accounts, and investment agency accounts. The Wealth Management Group may also serve as the personal representative of estates and act as trustee for revocable and irrevocable trusts.

The Bancorp's common stock is traded in the over the counter market and is quoted on the OTC Bulletin Board. On January 31, 2011, the Bancorp had 2,828,977 shares of common stock outstanding and 413 stockholders of record. This does not reflect the number of persons or entities who may hold their stock in nominee or “street” name through brokerage firms.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

General

The Bancorp's earnings are dependent upon the earnings of the Bank. The Bank's earnings are primarily dependent upon net interest margin. The net interest margin is the difference between interest income earned on loans and investments and interest expense paid on deposits and borrowings stated as a percentage of average interest earning assets. The net interest margin is perhaps the clearest indicator of a financial institution's ability to generate core earnings. Fees and service charges, wealth management operations income, gains and losses from the sale of assets, provisions for loan losses, income taxes and operating expenses also affect the Bancorp's profitability.

A summary of the Bancorp’s significant accounting policies is detailed in Note 1 to the Bancorp’s consolidated financial statements included in this report. The preparation of our financial statements requires management to make estimates and assumptions that affect our financial condition and operating results. Actual results could differ from those estimates. Estimates associated with the allowance for loan losses, fair values of foreclosed real estate, financial instruments and status of contingencies are particularly susceptible to material change in the near term as further information becomes available and future events occur.

At December 31, 2010, the Bancorp had total assets of $631.1 million and total deposits of $520.3 million. The Bancorp's deposit accounts are insured up to applicable limits by the Deposit Insurance Fund (DIF) that is administered by the Federal Deposit Insurance Corporation (FDIC), an agency of the federal government. At December 31, 2010, stockholders' equity totaled $56.1 million, with book value per share at $19.84. Net income for 2010 was $5.2 million, or $1.83 basic and diluted earnings per common share. The return on average assets was 0.77%, while the return on average stockholders’ equity was 9.03%.

Recent Developments

The Current Economic Environment. We continue to operate in a challenging and uncertain economic environment, including generally uncertain national conditions and local conditions in our markets. While overall economic activity appears to have stabilized to pre-recession levels, the growth rate is slow and national and regional unemployment rates remain at elevated levels not experienced in several decades. The risks associated with our business remain acute in periods of slow economic growth and high unemployment. Moreover, financial institutions continue to be affected by sharp declines in the real estate market and constrained financial markets. While we

are continuing to take steps to decrease and limit our exposure to problem loans, we nonetheless retain direct exposure to the residential and commercial real estate markets, and we are affected by these events.

Our loan portfolio includes residential mortgage loans, construction loans, and commercial real estate loans. Continued declines in real estate values, home sales volumes and financial stress on borrowers as a result of the uncertain economic environment, including job losses, could have an adverse effect on our borrowers or their customers, which could adversely affect our financial condition and results of operations. In addition, the current level of low economic growth on a national scale, the occurrence of another national recession, or further deterioration in local economic conditions in our markets could drive loan losses beyond that which are provided for in our allowance for loan losses and

result in the following other consequences: increases in loan delinquencies; problem assets and foreclosures may increase; demand for our products and services may decline; deposits may decrease, which would adversely impact our liquidity position; and collateral for our loans, especially real estate, may decline in value, in turn reducing customers’ borrowing power, and reducing the value of assets and collateral associated with our existing loans.

Impact of Recent and Future Legislation. Over the last 30 months, Congress and the U.S. Department of the Treasury (“Treasury”) have adopted legislation and taken actions to address the disruptions in the financial system and declines in the housing market, including the passage and implementation of the Emergency Economic Stabilization Act of 2008 (“EESA”), the Troubled Asset Relief Program (“TARP”), and the American Recovery and Reinvestment Act of 2009 (“ARRA”). In addition, on July 21, 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (the

“Dodd-Frank Act”), which significantly changes the regulation of financial institutions and the financial services industry.

The Dodd-Frank Act includes provisions affecting large and small financial institutions alike, including several provisions that will profoundly affect how community banks, thrifts, and small bank and thrift holding companies, such as the Bancorp, will be regulated in the future. Among other things, these provisions abolish the Office of Thrift Supervision and transfer its functions to the other federal banking agencies, relax rules regarding interstate branching, allow financial institutions to pay interest on business checking accounts, change the scope of federal deposit insurance coverage, and impose new capital requirements on bank and thrift holding companies. The Dodd-Frank Act also establishes the Bureau of

Consumer Financial Protection as an independent entity within the FRB, which will be given the authority to promulgate consumer protection regulations applicable to all entities offering consumer financial services or products, including banks. Additionally, the Dodd-Frank Act includes a series of provisions covering mortgage loan origination standards affecting, among other things, originator compensation, minimum repayment standards, and pre-payments. Moreover, the Dodd-Frank Act requires public companies like the Bancorp to hold shareholder advisory “say-on-pay” votes on executive compensation at least once every three years and submit related proposals to a vote of shareholders. However, the SEC has provided a temporary exemption for smaller reporting companies, such as the Bancorp, from the requirement to hold “say-on-pay” votes until the first annual or

other shareholder meeting occurring on or after January 21, 2013. The Dodd-Frank Act contains numerous other provisions affecting financial institutions of all types, many of which may have an impact on the operating environment of the Bancorp in substantial and unpredictable ways.

Consequently, the Dodd-Frank Act is likely to affect our cost of doing business, it may limit or expand our permissible activities, and it may affect the competitive balance within our industry and market areas. The nature and extent of future legislative and regulatory changes affecting financial institutions, including as a result of the Dodd-Frank Act, is very unpredictable at this time. The Bancorp’s management continues to actively review the provisions of the Dodd-Frank Act, many of which are phased-in over the next several months and years, and assess its probable impact on the business, financial condition, and results of operations of the Bancorp. However, the ultimate effect of the

Dodd-Frank Act on the financial services industry in general, and the Bancorp in particular, is uncertain at this time.

Moreover, it is not clear at this time what long-term impact the EESA, TARP, the ARRA, other liquidity and funding initiatives of the Treasury and other bank regulatory agencies that have been previously announced, and any additional programs that may be initiated in the future, will have on the financial markets and the financial services industry. The actual impact that EESA and such related measures undertaken to alleviate the credit crisis will have generally on the financial markets is unknown. The failure of such measures to help provide long-term stability to the financial markets could materially and adversely affect our business, financial

condition, results of operations, access to credit or the trading price of our common stock. Finally, there can be no assurance regarding the specific impact that such measures may have on the Bancorp, or whether (or to what extent) the Bancorp will be able to benefit from such programs. In addition to the legislation mentioned above, federal and state governments could pass additional legislation responsive to current conditions. For example, the Bancorp could experience higher credit losses because of federal or state legislation or regulatory action that reduces the amount the Bancorp’s borrowers are otherwise contractually required to pay under existing loan contracts. Also, the Bancorp could experience higher credit losses because of federal or state legislation or regulatory action that limits its ability to foreclose on property or other collateral or makes

foreclosure less economically feasible.

Difficult Market Conditions Have Adversely Affected Our Industry. We are particularly exposed to downturns in the U.S. housing market. Dramatic declines in the housing market over the past four years, with falling home prices and increasing foreclosures, unemployment and under-employment, have negatively impacted the credit performance of mortgage and construction loans and securities and resulted in significant write-downs of asset values by financial institutions, including government-sponsored entities, major commercial and investment banks, and regional financial institutions. Reflecting concern about the

stability of the financial markets generally and the strength of counterparties, many lenders and institutional investors have reduced or ceased providing funding to borrowers, including to other financial institutions. This market turmoil and tightening of credit have led to an increased level of commercial and consumer delinquencies, lack of consumer confidence, and increased market volatility. A worsening of these conditions would likely exacerbate the adverse effects of these difficult market conditions on the Bancorp and others in the financial institutions industry. In particular, the Bancorp may face the following risks in connection with these events:

|

|

•

|

We expect to face increased regulation of our industry, particularly in connection with the regulatory overhaul provisions of the Dodd-Frank Act. Compliance with such regulation may increase our costs and limit our ability to pursue business opportunities.

|

|

|

•

|

Our ability to assess the creditworthiness of our customers may be impaired if the models and approaches we use to select, manage and underwrite our customers become less predictive of future behaviors.

|

|

|

•

|

The process we use to estimate losses inherent in our credit exposure requires difficult, subjective and complex judgments, including forecasts of economic conditions and how these economic predictions might impair the ability of our borrowers to repay their loans, which may no longer be capable of accurate estimation which may, in turn, impact the reliability of the process

|

|

|

•

|

Our ability to borrow from other financial institutions on favorable terms or at all could be adversely affected by disruptions in the capital markets or other events, including actions by rating agencies and deteriorating investor expectations.

|

|

|

•

|

Competition in our industry could intensify as a result of the increasing consolidation of financial services companies in connection with current market conditions.

|

|

|

•

|

We may be required to pay significantly higher deposit insurance premiums because market developments have significantly depleted the insurance fund of the Federal Deposit Insurance Corporation (FDIC) and reduced the ratio of reserves to insured deposits.

|

In addition, the Federal Reserve Bank has been injecting vast amounts of liquidity into the banking system to compensate for weaknesses in short-term borrowing markets and other capital markets. A reduction in the Federal Reserve’s activities or capacity could reduce liquidity in the markets, thereby increasing funding costs to the Bancorp or reducing the availability of funds to the Bancorp to finance its existing operations.

Concentrations of Real Estate Loans Could Subject the Bancorp to Increased Risks in the Event of a Protracted Real Estate Recession. A significant portion of the Bancorp’s loan portfolio is secured by real estate. The real estate collateral in each case provides an alternate source of repayment in the event of default by the borrower and may deteriorate in value during the time the credit is extended. While real estate values in some regions of the country, including the Midwest, have shown signs of stabilizing, the real estate markets in many other regions of the country, most notably the West and Northeast, continue to show weakness, and a further

weakening of the real estate market could result in

an increase in the number of borrowers who default on their loans and a reduction in the value of the collateral securing their loans, which in turn could have an adverse effect on our profitability and asset quality. If we are required to liquidate the collateral securing a loan to satisfy the debt during a period of reduced real estate values, our earnings and capital could be adversely affected.

Financial Condition

During the year ended December 31, 2010, total assets decreased by $30.8 million (4.6%), to $631.1 million, with interest-earning assets decreasing by $25.3 million (4.1%). At December 31, 2010, interest earning assets totaled $586.0 million and represented 92.9% of total assets. Loans totaled $418.7 million and represented 71.4% of interest-earning assets, 66.3% of total assets and 80.5% of total deposits. The loan portfolio, which is the Bancorp’s largest asset, is a significant source of both interest and fee income. The Bancorp’s lending strategy emphasizes quality growth, product diversification, and competitive and profitable pricing. The loan

portfolio includes $152.9 million (36.5%) in residential real estate loans, $138.5 million (33.1%) in commercial real estate loans, $46.4 million (11.1%) in construction and land development loans, $61.7 million (14.7%) in commercial business loans, $10.4 million (2.5%) in government and other loans, $7.6 million (1.8%) in multifamily loans, $0.8 million (0.2%) in consumer loans, and $0.4 million (0.1%) in loans held for sale. Adjustable rate loans comprised 40.7% of total loans at year-end. During 2010, loan balances decreased by $40.6 million (8.8%), with commercial real estate loan balances increasing, while construction and development, residential real estate, government, multifamily, consumer, and loans held for sale balances decreased. The decrease in loans during the year is partially the result of management’s interest rate risk reduction strategy of selling fixed rate

mortgage loans to the secondary market.

The Bancorp is primarily a portfolio lender. Mortgage banking activities are generally limited to the sale of fixed rate mortgage loans with contractual maturities greater than 15 years. However, as a result of the low interest rate environment, during 2010, management sold newly originated fixed rate mortgage loans with maturities ranging from 10 to 30 years in an effort to minimize future interest rate risk. These loans are identified as held for sale when originated and sold, on a case-by-case basis, in the secondary market. During 2010, the Bancorp sold $36.3 million in newly originated fixed rate mortgage loans, compared

to $49.4 million during 2009. During the current year, the continued loan sale activity was a result of the Federal Reserve’s sustained effort to maintain a low interest rate environment. Lower long-term interest rates also created mortgage loan refinance opportunities for borrowers within the Bancorp’s market area. In addition, during the fourth quarter of 2010, the Bancorp conducted a $5.1 million one-time sale of portfolio fixed rate mortgage loans, which were sold to reduce interest rate risk. Net gains realized from mortgage loan sales totaled $1.3 million for 2010, compared to $1.1 million for 2009. At December 31, 2010, the Bancorp had $422 thousand in loans that were classified as held for sale.

The allowance for loan losses (ALL) is a valuation allowance for probable incurred credit losses, increased by the provision for loan losses, and decreased by charge-offs, less recoveries. A loan is charged off against the allowance by management as a loss when deemed uncollectible, although collection efforts continue and future recoveries may occur. The determination of the amounts of the ALL and provisions for loan losses are based on management’s current judgments about the credit quality of the loan portfolio with consideration given to all known relevant internal and external factors that affect loan collectability as of the reporting date. The

appropriateness of the current year provision and the overall adequacy of the ALL are determined through a disciplined and consistently applied quarterly process that reviews the Bancorp’s current credit risk within the loan portfolio and identifies the required allowance for loan losses given the current risk estimates.

Historically, the Bancorp has successfully originated commercial real estate loans within its primary lending area. However, beginning in the fourth quarter of 2005, in a response to a decrease in local loan demand and in an effort to reduce the potential credit risk associated with geographic concentrations, a strategy was implemented to purchase commercial real estate participation loans outside of the Bancorp’s primary lending area. The strategy to purchase these commercial real estate participation loans was limited to 10% of the Bancorp’s loan portfolio. The Bancorp’s management discontinued the strategy during the third

quarter of 2007. As of December 31, 2010, the Bancorp’s commercial real estate participation loan portfolio carried an aggregate balance of $28.9 million. Of the $28.9 million in commercial real estate participation loans, $9.0 million has been purchased within the Bancorp’s primary lending area and $19.9 million outside of the primary lending area. At December 31, 2010, $14.5 million, or 50.2%, of the Bancorp’s commercial real estate participation loans have been internally classified as substandard and have been placed on non-accrual status. Of the $14.5 million in substandard commercial real estate participation loans placed on non-accrual status, $12.1 million are located outside of the Bancorp’s primary lending area. The discussion in the paragraphs that follow regarding non-performing loans, internally classified loans and impaired

loans include loans from the Bancorp’s commercial real estate participation loan portfolio.

For all of its commercial real estate participation loans, the Bancorp’s management requires that the lead lenders obtain external appraisals to determine the fair value of the underlying collateral for any collateral dependent loans. The Bancorp’s management requires current external appraisals when entering into a new lending relationship or when events have occurred that materially change the assumptions in the existing appraisal. The lead lenders receive external appraisals from qualified appraisal firms that have expertise in valuing commercial properties and are able to comply with the required scope of the engagement. After the lead lender receives the external appraisal and performs its

compliance review, the appraisal is forwarded to the Bancorp for review. The Bancorp’s management validates the external appraisal by conducting an in-house review by

personnel with expertise in commercial real estate developments. If additional expertise is needed, an independent review appraiser is hired to assist in the evaluation of the appraisal. The Bancorp is not aware of any significant time lapses during this process. Periodically, the Bancorp’s management may make adjustments to the external appraisal assumptions if additional known quantifiable data becomes available that materially impacts the value of a project. Examples of adjustments that may occur are changes in property tax assumptions or changes in capitalization rates. The Bancorp’s management relies on up-to-date external appraisals to determine the current value of

its commercial real estate participation loans. These values are appropriately adjusted to reflect changes in market value and, when necessary, are the basis for establishing the appropriate allowance for loan losses. If an updated external appraisal for a commercial real estate participation loan is received after the balance sheet date, but before the annual or quarterly financial statements are issued, material changes in appraised values are “pushed back” in the yet to be issued financial statements in order that appropriate loan loss provision is recorded for the current reporting period. The Bancorp’s management consistently records loan charge-offs based on the fair value or income approach of the collateral as presented in the current external appraisal.

Non-performing loans include those loans that are 90 days or more past due and those loans that have been placed on non-accrual status. Non-performing loans totaled $24.1 million at December 31, 2010, compared to $18.6 million at December 31, 2009, an increase of $5.5 million or 29.9%. The current level of non-performing loans is concentrated with five commercial real estate participation loans in the aggregate of $14.5 million. As previously reported, one commercial real estate participation loan is a condominium construction project in Orlando, Florida, with a current balance of $1.5 million, which is classified as substandard. The carrying value of this

loan is based on the current fair value of the project’s collateral, less estimated selling costs. The second commercial real estate participation loan is an end loan for a hotel located in Dundee, Michigan, with a current balance of $1.2 million, which is classified as substandard. The carrying value of this loan is based on the current fair value of the hotel, less estimated selling costs. The third commercial real estate participation loan is an end loan for a hotel located in Fort Worth, Texas, with a balance of $5.0 million, which is classified as substandard. The carrying value of this loan is based on the current fair value of the hotel, less estimated selling costs. The fourth commercial real estate participation loan was placed on non-accrual status during the third quarter of 2010. This loan is a hotel construction project located in Clearwater, Florida, with a balance

of $4.4 million, which is classified as substandard. The carrying value of this loan is based on the current fair value of the project, less estimated selling costs. The fifth commercial real estate participation loan was placed on non-accrual status during the third quarter of 2010. This loan is a land development project located in Crown Point, Indiana, with a balance of $2.4 million, which is classified as substandard. The carrying value of this loan is based on the current fair value of the project, less estimated selling costs. For these commercial real estate participation loans, to the extent that actual cash flows, collateral values and strength of personal guarantees differ from current estimates, additional provisions to the allowance for loan losses may be required.

The ratio of non-performing loans to total loans was 5.77% at December 31, 2010, compared to 4.05% at December 31, 2009. The increase is primarily attributable to the previously mentioned five commercial real estate participation loans. The ratio of non-performing loans to total assets was 3.82% at December 31, 2010, compared to 2.81% at December 31, 2009. The December 31, 2010, non-performing loan balances include $24.0 million in loans accounted for on a non-accrual basis and $148 thousand in accruing loans, which were contractually past due 90 days or more. Loans, internally classified as substandard, totaled $32.7 million at December 31, 2010,

compared to $22.7 million at December 31, 2009. The current level of substandard loans includes the previously mentioned five non-accruing commercial real estate participation loans and one accruing commercial real estate hotel loan in the amount of $5.0 million. During October 2010, a $4.9 million accruing commercial real estate participation hotel loan that was classified as substandard and non-accrual received significant collateral enhancements. Additional liquid collateral was received in the amount of $1.4 million along with $2.0 million in payment reserves. As a result of sustained performance for principal and interest payments and the enhanced collateral position, management moved this loan from substandard to watch and accrual status during the fourth quarter of 2010. Substandard loans include non-performing loans and potential problem loans, where information about possible

credit issues or other conditions causes management to question the ability of such borrowers to comply with loan covenants or repayment terms. No loans were internally classified as doubtful or loss at December 31, 2010 or December 31, 2009. In addition to identifying and monitoring non-performing and other classified loans, management maintains a list of watch loans. Watch loans represent loans management is closely monitoring due to one or more factors that may cause the loan to become classified. Watch loans totaled $24.3 million at December 31, 2010, compared to $26.7 million at December 31, 2009.

A loan is considered impaired when, based on current information and events, it is probable that a borrower will be unable to pay all amounts due according to the contractual terms of the loan agreement. At December 31, 2010, impaired loans totaled $26.0 million, compared to $17.0 million at December 31, 2009. The December 31, 2010, impaired loan balances consist of twenty-five commercial real estate and commercial business loans that are secured by business assets and real estate, and are personally guaranteed by the owners of the businesses. The December 31, 2010 ALL contained $2.8 million in specific allowances for collateral deficiencies, compared to $1.2 million

in specific allowances at December 31, 2009. The increase in specific allowances is a result of the continued downward pressure on market valuations that are based on projected cash flows. During the fourth quarter of 2010, one additional commercial real estate loan totaling $585 thousand was newly classified as impaired. Management’s current estimate

indicates a collateral deficiency of $42 thousand for this loan. In addition, during the fourth quarter nine loans totaling $1.6 million were removed from impaired status, as a result of credit upgrades, transfers to foreclosed real estate, or charge-offs. As of December 31, 2010, all loans classified as impaired were also included in the previously discussed substandard loan balances. There were no other loans considered to be impaired loans as of December 31, 2010. Typically, management does not individually classify smaller-balance homogeneous loans, such as mortgage or consumer loans, as impaired.

At December 31, 2010, the Bancorp classified five loans totaling $12.1 million as troubled debt restructurings, which involves modifying the terms of a loan to forego a portion of interest or principal or reducing the interest rate on the loan to a rate materially less than market rates. The troubled debt restructurings are comprised of one construction development participation hotel loan in the amount of $1.2 million, for which a significant deferral of principal repayment was granted. The second troubled debt restructuring is for a commercial real estate participation hotel loan in the amount of $5.0 million, for which a significant deferral of principal repayment and extension in maturity was granted. The third

is for a commercial real estate hotel loan in the amount of $5.0 million for which a significant deferral of principal repayment was granted. This loan is on accrual status and classified as impaired. In addition, two commercial real estate troubled debt restructurings in the total amount of $893 thousand are currently in bankruptcy proceedings, for which a significant deferral of principal and interest repayment was granted by the Bank as required by the bankruptcy plan. All of the loans classified as troubled debt restructurings are currently on non-accrual status and classified as impaired except for one loan, which is on accrual status. The valuation basis for the Bancorp’s troubled debt restructurings is based on the present value of cash flows, unless consistent cash flows are not present, then the fair value of the collateral securing the loan is the basis for

valuation.

At December 31, 2010, management is of the opinion that there are no loans, except those discussed above, where known information about possible credit problems of borrowers causes management to have serious doubts as to the ability of such borrowers to comply with the present loan repayment terms and which may result in disclosure of such loans as non-accrual, past due or restructured loans. Management does not presently anticipate that any of the non-performing loans or classified loans would materially impact future operations, liquidity or capital resources.

For 2010, $5.6 million in provisions to the ALL were required, compared to $8.5 million for 2009. The ALL provision decrease for 2010 is a result of lower charge-off activity for the Bancorp’s commercial real estate participation loans. The current year ALL provisions were related to the elevated credit risk in the commercial real estate participation, commercial real estate and commercial business loan portfolios. Charge-offs, net of recoveries, totaled $2.6 million for 2010, compared to $7.1 million for 2009. The 2010 net loan charge-offs of $2.6 million were comprised of $720 thousand in commercial real estate participation loans, $919 thousand in commercial

real estate loans, $727 thousand in residential real estate loans, $172 thousand in commercial business loans and $25 thousand in consumer loans. The ALL provisions take into consideration management’s current judgments about the credit quality of the loan portfolio, loan portfolio balances, changes in the portfolio mix and local economic conditions. In determining the provision for loan losses for the current period, management has given consideration to increased risks associated with the local economy, changes in loan balances and mix, and asset quality.

The ALL to total loans was 2.18% at December 31, 2010, compared to 1.33% at December 31, 2009. The increase in ALL to total loans was a result of the increase in substandard and non-performing loans, and additional qualitative risks associated with the current stressed economic environment. The ALL to non-performing loans (coverage ratio) was 37.8% at December 31, 2010, compared to 32.9% at December 31, 2009. The December 31, 2010 balance in the ALL account of $9.1 million is considered adequate by management after evaluation of the loan portfolio, past experience and current economic and market conditions. While management may periodically

allocate portions of the allowance for specific problem loans, the whole allowance is available for any loan charge offs that occur. The allocation of the ALL reflects performance and growth trends within the various loan categories, as well as consideration of the facts and circumstances that affect the repayment of individual loans, and loans which have been pooled as of the evaluation date, with particular attention given to non-performing loans and loans which have been classified as substandard, doubtful or loss. Management has allocated reserves to both performing and non-performing loans based on current information available.

At December 31, 2010, the Bancorp's investment portfolio totaled $160.5 million and was invested as follows: 61.1% in U.S. government agency mortgage-backed securities and collateralized mortgage obligations, 35.4% in municipal securities, 2.6% in U.S. government agency debt securities, and 0.9% in trust preferred securities. At December 31, 2010, securities available-for-sale totaled $142.1 million or 88.5% of total securities. Available-for-sale securities are those the Bancorp may decide to sell if needed for liquidity, asset-liability management or other reasons. During 2010, securities increased by $16.1 million (11.2%). In addition, at December 31, 2010, the

Bancorp had $3.4 million in FHLB stock.

As of December 31, 2010, the Bancorp’s management was notified that the quarterly interest payments for three of its four investments in trust preferred securities are in “payment in kind” status. Payment in kind status results in a temporary delay in the payment of interest. As a result of a delay in the collection of the interest payments, management placed these securities on non-accrual status. At December 31, 2010, the cost basis of the three trust preferred securities on non-accrual status totaled $3.9 million. Current estimates indicate that the interest payment delays may exceed ten years. One trust preferred security with a cost

basis of $1.3 million remains on accrual status.

Deposits are a fundamental and cost-effective source of funds for lending and other investment purposes. The

Bancorp offers a variety of products designed to attract and retain customers, with the primary focus on building and expanding relationships. At December 31, 2010, deposits totaled $520.3 million. During 2010, deposits decreased by $20.3 million (3.7%). The 2010 change in deposits was comprised of the following: certificates of deposit decreased by $28.4 million (12.5%), checking accounts decreased by $3.0 million (2.1%), money market deposit accounts (MMDA’s) increased by $2.9 million (2.6%), while savings accounts increased by $8.2 million (14.5%). During 2010, as a result of carrying excess liquidity, management implemented a strategy that allowed for the reduction in higher cost certificates of deposit.

The increase in MMDA and savings balances is a result of customer preferences for liquid investments in the current low interest rate environment.

The Bancorp’s borrowed funds are primarily comprised of repurchase agreements and FHLB advances that are used to fund asset growth not supported by deposit generation. At December 31, 2010, borrowed funds totaled $48.6 million compared to $63.0 million at December 31, 2009, a decrease of $14.4 million (22.9%). During 2010, management repaid borrowed funds with excess liquidity. Retail repurchase agreements totaled $16.1 million at December 31, 2010, compared to $15.9 million at December 31, 2009, an increase of $0.2 million (1.2%). FHLB advances totaled $29.0 million, decreasing $9.0 million or 23.7%. In addition, the Bancorp’s FHLB line of

credit carried a balance of $3.2 million at December 31, 2010, compared to $8.5 million at December 31, 2009. Other short-term borrowings totaled $296 thousand at December 31, 2010, compared to $664 thousand at December 31, 2009.

Liquidity and Capital Resources

The Bancorp’s primary goal for funds and liquidity management is to ensure that at all times it can meet the cash demands of its depositors and its loan customers. A secondary purpose of funds management is profit management. Because profit and liquidity are often conflicting objectives, management will maximize the Bank’s net interest margin by making adequate, but not excessive, liquidity provisions. Furthermore, funds are managed so that future profits will not be significantly impacted as funding costs increase.

Changes in the liquidity position result from operating, investing and financing activities. Cash flows from operating activities are generally the cash effects of transactions and other events that enter into the determination of net income. The primary investing activities include loan originations, loan repayments, investments in interest bearing balances in financial institutions, dividend receipts and the purchase and maturity of investment securities. Financing activities focus almost entirely on the generation of customer deposits. In addition, the Bancorp utilizes borrowings (i.e., repurchase agreements, FHLB advances and federal funds purchased) as a source of

funds.

During 2010, cash and cash equivalents decreased $2.3 million compared to a increase of $1.9 million for 2009. During 2010, the primary sources of cash and cash equivalents were from loan sales and repayments, maturities and sales of securities, FHLB advances, and cash from operating activities. The primary uses of cash and cash equivalents were loan originations, purchase of securities, expenditures for premises and equipment, decrease in deposits, FHLB advance repayments and the payment of common stock dividends. During 2010, cash from operating activities totaled $14.5 million, compared to $1.2 million for 2009. The 2010 increase in cash provided by operating

activities was a result of higher net income, having prepaid three years of FDIC assessments in 2009, and ACH prefunding liabilities. Cash inflows from investing activities totaled $19.9 million during 2010, compared to $3.3 million during 2009. The change for the current year was related to a decrease in loan balances, maturities and pay downs of AFS securities, and foreclosed real estate sales. Loan sales totaled $41.4 million for 2010, compared to $60.0 million in 2009. Net cash outflows from financing activities totaled $36.7 million in 2010, compared to net cash outflows of $2.7 million in 2009. The change during 2010 was primarily due to a decrease in deposits. Deposits decreased by $20.3 million during 2010, compared to an increase of $12.4 million for 2009. FHLB advances decreased by $9.0 million during 2010 compared to an $8.0 million increase during 2009. The lower deposit

growth and reduction in advance balances was a result of lower funding requirements during 2010. The Bancorp paid dividends on common stock of $2.2 million and $3.4 million during 2010 and 2009, respectively. During 2010, the Bancorp’s Board of Directors reduced dividends to build capital and preserve long-term capital strength.

During the third quarter of 2010, the Bancorp opened its twelfth full service banking center in Saint John, Indiana. The new $2.1 million state-of-the-art facility did not have a material impact on operations during 2010. It is expected that the new banking center will provide opportunities to expand market share for the Bancorp’s products and services.